Elder Care & Estates

Elder Care Advance Planning *SEE NOTES 1 & 2 BELOW

Long-term Care Planning *SEE NOTES 1 & 2 BELOW

$ Monetary Services *SEE NOTES 1 & 2 BELOW

Business Restructuring, Mergers, Acquisitions & Business Sale

Annuities *SEE NOTES 1 & 2 BELOW

NOTE 1 - ALL TRANSACTION MATTERS THAT PERTAIN TO SECURITIES (INCLUDING BONDS); INSURANCE OF ANY KIND; ANNUITIES ETC. WILL BE HANDLED THRU CETERA FINANCIAL ADVISORS AND WILL NOT IN ANY WAY BE HANDLED THRU SY SCHNUR, CPA & ASSOCIATES WHICH IS AN ACCOUNTING FIRM ONLY. ANY INFORMATION SUBMITTED THRU OUR ACCOUNTING WEBSITES WILL BE FORWARDED TO OUR SISTER SITE SYFINANCE.COM.

NOTE 2 - SECURITIES AND INSURANCE SERVICES ARE OFFERED ONLY THROUGH CETERA FINANCIAL SPECIALISTS LLC. MEMBER FINRA & SIPC. ADVISORY SERVICES IS OFFERED ONLY THRU CETERA INVESTMENT ADVISERS LLC. CETERA ENTITIES ARE UNDER SEPARATE OWNERSHIP FROM EVERY OTHER ENTITY.

Elder Care Advance Planning

ElderCare/PrimePlus Glossary

401(K) Plans – A 401(k) is a tax-deferred investment and savings plan that acts as a personal pension fund for employees. It allows employees of corporations and private companies to save and invest for their own retirement. In a 401(k) the employee authorizes pre-tax payroll deductions to be invested in mutual funds or other investment options offered by the employer's plan. Often, employers match the employee's contributions. The contributions, the investment earnings, and any employer match may grow tax-deferred until withdrawal (assumed to be retirement), at which time they are taxed as ordinary income. Like 403(b), assets in IRAs can be withdrawn without penalty after age 59? and must start no later than April 1 of the year following the date that one turns age 70? and be taken annually subject to minimum distribution requirements.

403(B) Plans – A 403(b) is a tax-deferred investment and savings program for employees of certain tax-exempt employers. It allows employees of hospitals, educational institutions, and other non-profit organizations to save and invest for their own retirement. Depending on the program, an employee authorizes pre-tax payroll deductions to be invested in a tax-sheltered annuity (TSA) or in a custodial account made up of mutual funds offered by the employer. Both contributions and the investment earnings may grow tax-deferred until withdrawal (assumed to be retirement), at which time they are taxed as ordinary income. Like IRAs, assets in a 403(b) can be withdrawn without penalty after age 59? and must start no later than April 1 of the year following the date that one turns age 70? and be taken annually subject to minimum distribution requirements.

Abuse – Physical and Emotional – Physical and emotional abuse includes neglect, abandonment, beating, restraint, deprivation of food or water, sexual abuse, humiliation, intimidation, insults, threats, and harassment. Abuse may be domestic, institutional, or self neglect.

ADL – The term "activities of daily living," or ADL’s, refers to the basic tasks of everyday life, such as eating, bathing, dressing, toileting, and transferring. When people are unable to perform these activities, they need help in order to cope, either from other human beings, mechanical devices or both. Although people of all ages may have problems performing the ADLs, prevalence rates are much higher for the elderly than for the non-elderly. Within the elderly population, ADL prevalence rates rise steeply with advancing age and are especially high for a person aged 85 and over. Measurement of the activities of daily living is critical because they have been found to be significant predictors of admission to a nursing home; use of paid home care; use of hospital services; use of physician services; trigger of insurance coverage and mortality.

Alzheimer’s Disease – Alzheimer’s disease (AD) is the most common cause of dementia in older people. AD affects the parts of the brain that control thought, memory, and language. It is a slow disease that starts with mild memory problems and leads to severe brain damage. People with AD lose their abilities at different rates. AD can last from 3 to 20 years or more after the onset of symptoms. It is not yet clear what causes AD and there is no known cure. The behavioral problems in AD are not something the person can control. They result from the brain damage that worsens over time. AD begins slowly. At first, the only symptom may be memory problems. People with AD may have trouble remembering recent events, activities, or the names of familiar people or things.

They may ask the same question over and over again. Simple math problems may become hard to solve. Such difficulties begin to interfere with jobs or other activities. As the disease gets worse, people with AD may:

• Forget something that just happened even though they can remember events from many

years ago.

• Become disoriented and get lost in familiar places.

• Become passive and lose their initiative.

• Forget how to do simple tasks like brushing their teeth or combing their hair.

• Not be able to think clearly.

• Have trouble talking, understanding, reading, and writing.

• Stop bathing regularly or eating regular meals.

• Have sudden, unpredictable mood changes.

• Become suspicious and paranoid about other people's intentions and behavior.

• Become confused, anxious or aggressive. Some may become violent or angry, while others may be docile or helpless.

• Wander away from home

• Eventually, persons with AD need total care.

Clients are very concerned about the financial ramifications of getting Alzheimer’s—they’re just not doing anything about it.

A recent survey performed by WebMD entitled “Insight Into Alzheimer’s Attitudes and Behaviors” polled 4,200 site users about their fears, beliefs and experiences with the disease. The results reveal that Alzheimer’s planning is a need that’s going unmet—and an opportunity for advisors to add value. Click here to read more.

Assisted Living Facility – Assisted living is a combination of housing and health care services for individuals needing assistance with some of the activities of daily living (eating, walking, bathing, etc.). Assisted living is a general term for living arrangements in which some services are available to residents (e.g., meals, cleaning, and medication reminders), but residents still live independently within the assisted living complex.

• The first is independent living in a small home on the grounds. The home might be a patio home, a condominium, a cottage, a ranch home, or even an apartment in a high-rise building. In many CCRCs there is a choice between renting an apartment or buying a home. Residents of these facilities are normally in fairly good health and lead quite independent lives, coming and going as they please.

• The second phase of a CCRC is an assisted living facility. Residents receive some help with daily living and dressing, for example. Depending on the facility, the resident may just have a room and bathroom, or an apartment with a small kitchen. In any event, there is always a dining room where the resident(s) may take meals if they so choose.

• The third phase of a CCRC is a nursing home, which offers 24-hour skilled care. Each CCRC is different, with its own appearance, rules and regulations, health care coverage, and cost. Some will only allow an individual to move in during the independent living phase.

Death Benefits – Money and/or in-kind benefits paid to the survivors of the deceased (also called survivor benefits). These benefits are usually provided to eligible survivors of the deceased upon receipt of proof of death, such as a copy of the death certificates. Amounts may be paid in one lump sum, as in life insurance policies and the Social Security lump-sum burial expense payment, or they may be paid over time, as in Social Security survivor benefits.

Dementia – Dementia refers to a group of symptoms that are caused by changes in brain function. Signs of dementia include changes in memory, personality, and behavior. Dementia makes it hard for a person to carry out normal daily activities. A person with dementia may ask the same questions repeatedly and get lost in familiar places. He or she may be unable to follow directions; be disoriented about time, people, and places; and neglect personal safety, hygiene, and nutrition. Older people with dementia were once called senile, and it was thought that becoming senile was just part of getting old. But dementia is not a normal part of aging. It is important to find out the cause of a person's dementia. Some causes of dementia can be treated and reversed. Others are due to irreversible changes in the brain and cannot be cured.

Funeral Rule – This rule requires funeral homes to give consumers accurate, itemized price information and various other disclosures about funeral goods and services. The Federal Trade Commission's Funeral Rule applies to pre-need and at-need funeral arrangements. The key to the FTC Funeral Rule is the "General Price List." The General Price List should be printed or typewritten, and must contain the following identifying information:

• The name, address, and telephone number of the funeral provider’s place of business, including (where relevant) the address and telephone number for each branch;

• The caption: "General Price List;"and

• The effective date of the price list.

The following three disclosures must appear on the Statement. They should be set out, word-for word, exactly as the Rule prescribes. They are 1) Legal Requirements; 2) Embalming; and 3) Cash Advance Items.

The Funeral Rule prohibits specific misrepresentations in six areas: embalming, Casket for Direct Cremation, Outer Burial Container, Legal and Cemetery Requirements, Preservative and Protective Value Claims and Cash Advance Items.

Geriatric Care Manager [GCM] – Generally, a geriatric care manager is a person who

develops and implements a plan for all aspects of long-term care to assist an elderly person and, indirectly, the person's family members upon whose shoulders this task would otherwise fall. Although not required, a geriatric care manager will have some form of graduate degree, social work and nursing seem to be the most common, and may be (although not required) certified or licensed by a professional organization or by state statute or regulations.

Guardianship – The legal relationship between a ward and a guardian – wards are usually persons who have been declared incompetent by the courts to make particular decisions on their own behalf. Court appointed guardians act as surrogate decision makers for the ward.

Home Care – Services provided in the home to promote, maintain and restore health or to minimize the effects of illness and disability. Home care can be for short-term purposes, such as rehabilitative care after a hospital discharge or care for the terminally ill or for long-term purposes, such as assistance with activities of daily living for person with chronic disabilities.

Home Health Benefits – If an individual is homebound and requires skilled services on an intermittent basis, Medicare will cover up to 35 hours per week of home health aide and skilled nursing services. Skilled-nursing services include the administration of medication, IV therapy, tube feedings, catheter changes, and wound care. Intermittent usually means less than five days per week, but certain people may receive services seven days per week.

Hospice Care – A hospice is a public agency or private organization that is primarily engaged in providing pain relief, symptom management, and supportive services to terminally individuals. Hospice care includes both home and inpatient care. Under the Medicare hospice benefit, Medicare covers costs of daily care and permits a hospice to provide appropriate custodial care, including homemaker services and counseling.

Individual Retirement Accounts (IRAs) – An IRA is a tax-deferred investment and savings account that acts as a personal retirement fund for people with employment income. In a traditional IRA contributions may be deductible or non-deductible, and the earnings may grow tax-deferred until withdrawal (assumed to be retirement), at which time they are taxed as ordinary income. IRAs are designed for individuals with earned income or married couples in which only one of the spouses has earned income and the couple files a joint return. (See Roth IRA.)

Inter Vivos or Living Trust – In this type of trust generally established as a revocable trust, the maker places his/her assets into the trust and is the trustee of the trust. A successor trustee may manage those assets if the maker of the trust becomes incapacitated and will distribute the assets of the trust when the maker dies. The successor trustee is the fiduciary, and has a legal duty to follow the terms of the trust as set out by the maker. This type of trust may allow the maker to avoid probate at death and conservatorship in the event of incapacity.

Keogh Plans – A Keogh is a tax-deferred retirement plan designed to help self-employed workers or individuals who earn self-employed income establish a retirement savings program.

There are two different types of Keogh’s, profit-sharing or money purchase plan. Under Keogh regulations the money purchase plan contribution is mandatory and the same percentage contribution is made each year, whether there are profits or not. The profit sharing contribution may change each year, and individuals may contribute to both types of plans in the same year. The most attractive feature of Keogh plans is the high maximum contribution (currently up to $44,000) and it will now be indexed for inflation. The self-employed person makes contributions, and these along with investment earnings grow tax-deferred until withdrawal (assumed to be retirement), at which time they are taxed as ordinary income

Last Will and Testament – A Will is perhaps the most well-known means of disposing of property at death. Every state has its own rules for the making of a valid Will, but at the very least, they involve a written document that is

1. Signed by the person making it (called the testator or, if female, the testatrix), and

2. Witnessed by at least two disinterested witnesses (those who do not stand to inherit under the Will.)

The person nominated by the testator to wind down the affairs of the decedent is called the executor or, if female, the executrix. When a person with a Will dies, he/she is said to die testate. This means, simply, that the Will governs the disposition of that person's property. The "alternative" to dying testate is dying intestate. A person dying intestate has no Last Will and Testament.

Living Wills – A living will is a directive to physicians allowing an individual to express his or her desire not to be kept alive by extraordinary means in the event he or she is determined to be in a terminal condition. This document directs the physician to give or withhold life sustaining medical care. The principal should state in the living will the conditions under which treatments should be continued or discontinued and what types of life sustaining efforts should be made.

Long-Term Care Insurance – Long-term care insurance covers an individual for many of the costs of home health care, the costs of community-based care (such as assisted

living) and, the costs of nursing home care. It rarely covers the costs of medical care – doctors or hospitals. This coverage works in conjunction with Medicare and/or private health insurance. A long-term care insurance policy is a contract between an individual and an insurance company. In exchange for the payment of premiums, the insurance company provides for the payment of a daily benefit to cover the costs of long-term care.

Lump-Sum Death Benefit – When a Social Security recipient dies, a lump-sum death benefit is payable either to the surviving spouse or to a qualifying child [42 USC §402(I)]. A qualifying child is one who was entitled to receive benefits as a result of the wage-earner’s Social Security benefits.

Medicaid – Medicaid is a medical assistance program intended for those who have no other means to pay for necessary health care services. Entitlement is based on need alone and no premium payments are required. Medicaid is primarily administered by the states with a federal contribution that ranges between 50% and 80% of the funds paid out by the state for Medicaid services. Although specific regulations governing Medicaid vary from state to state, each state must comply with strict requirements in the Medicaid statute regarding eligible services, eligibility of participants, estate recovery, and other matters.

Medicaid for Long-Term Care – Medicaid may be used to supplement Medicare for what is sometimes referred to as "community Medicaid benefits." Community benefits are traditional medical services delivered by physicians, hospitals, and other health care providers outside of nursing homes.

Medicare – Medicare is a federal health insurance program for people aged 65 and older, those with certain disabilities, some under 65, and people of any age who suffer from permanent kidney failure. It is intended to provide basic insurance protection against health care costs, not to cover all medical expenses or long-term care. An eligible individual may choose to get benefits under Medicare through the traditional fee-for-service system (sometimes called Medicare) or through a managed care program, Medicare Choice. The traditional Medicare program has two parts. Part A is Hospital Insurance, and Part B is Supplementary Medical Insurance. Part A pays some of the costs of hospitalization, very limited nursing home care, and some home health services. Part B primarily covers doctors' fees, most outpatient and certain related services. Part A is free to qualifying participants. A small monthly premium ($93.50 per month in 2007) is charged for Medicare Part B coverage. Medicare Advantage – As a result of legislation passed in 1997, beneficiaries could (starting in 1999) opt out of the "traditional" Medicare program in favor of a private managed care plan or private fee-for-service plans. Medicare had been experimenting with managed care, specifically HMOs, for some time prior to the adoption of this legislation and a large number of Medicare

beneficiaries have had coverage through HMOs for a number of years. To be eligible for

Medicare managed care plans an individual must

• Have both Part A (Hospital Insurance) and Part B (Medical Insurance) coverage,

• Not have end-stage renal (kidney) disease (unless they were already in a managed care

plan prior to the enactment of the legislation), and

• Live in the service area of a Medicare managed care plan.

Medicare Benefit Period – Deductible and co-payment amounts for Medicare Part A are determined per benefit period. A benefit period begins when a participant enters the hospital and continues until after the patient has been out of the hospital or skilled nursing care for 60 days. After that time, a new benefit period begins. Consequently, there may be several “benefit periods” in a year under Medicare Part A. Co-payments and deductibles under Medicare Part B and computed on an annual basis without

regard to the “benefit period” provided in Medicare Part A.

Medicare Claims Processors – Medicare claims processors are known as "fiscal intermediaries" and "carriers." Medicare intermediaries process hospital insurance (Part A) claims for institutional services, including inpatient hospital claims, skilled-nursing facilities, home health agencies, and hospice services. They also process hospital outpatient claims payable under supplementary medical insurance (Part B). Examples of fiscal intermediaries are the Blue Cross and Blue Shield Association and commercial insurance companies.

Medicare Supplemental Insurance (Medigap) – Traditional Medicare coverage does not pay all medical expenses. There are deductibles, coinsurance amounts, non-allowable charges, and non-covered services. If an individual is covered through the traditional Medicare program, additional health insurance is needed to fill the gaps in coverage. Many retired persons and/or their spouses have protection that is provided by their former employer. Others purchase supplementary insurance policies, referred to as Medigap insurance.

Pension Plans – This is a traditional retirement plan offered by some employers that pays a set amount each year during retirement. Also called a defined-benefit plan, company pensions guarantee a specific amount of benefits to employees, calculated using a formula that typically includes the employee's final salary, years of service, and a fixed percentage rate.

Powers of Attorney – Simply put, a power of attorney is a document whereby one person (called the "principal") authorizes someone else (called the "agent," or the "attorney-in-fact") to act on his/her behalf. A power of attorney may be “general,” granting broad authority to make decisions concerning investments, tax matters, and property transactions, or it may be “specific,” granting only limited authority to perform one of more specific duties. Every state has legislation authorizing the creation and use of powers of attorney. In all cases, the principal must be competent when the power of attorney is executed.

Note: There are different kinds of powers of attorney – also called advanced directives.

PrimePlus Services – The ElderCare Services brand is transitioning to PrimePlus Services to make it easier for clients to see the connection between traditional services and the more global approach to the services that older clients need. The new focus on PrimePlus Services leverages existing strengths and competencies in cash flow planning and budgeting, pre- and postretirement planning, insurance reviews and tax planning. The new positioning allows CPAs to broaden their focus to include pre-retirement age clients, and to benefit from the greater revenue potential of this expanded market and from the longer term of the potential revenue stream.

Roth IRAs – The Taxpayer Relief Act of 1997 introduced a new option for IRAs, the Roth IRA. The Roth IRA offers higher income limits and more relaxed eligibility rules than available with a traditional IRA. In addition to these differences the Roth IRA turns the traditional IRA formula on its head. Retirement contributions are not deductible up front, but withdrawals can be made tax-free after age 59?.

Skilled-Nursing Facility Benefits – Medicare provides up to 100 days of care in a Medicare certified skilled-nursing facility (SNF) per benefit period (as defined above) if the individual was an inpatient in an acute care hospital for at least 3 days during the 30 days immediately prior to admission to the SNF and it has been determined they are in need of daily skilled services. Medicare defines "daily" as needing seven days per week of skilled-nursing care and at least five days per week of skilled therapy. Medicare pays for the first 20 days in a SNF. For days 21 through 100 a co-insurance amount ($109.50 per day in 2004-3) is due. Note: The dollar information is subject to change; practitioners should update their references as changes are issued.

Social Security – Individuals qualify for Social Security retirement benefits as early as age 62 if they have held a job and paid Social Security taxes for at least 10 years. It provides monthly cash benefits to retirees and their dependents, to disabled workers and their dependents and to surviving dependents of deceased workers and retirees.

Statement of Funeral Goods and Services Selected – The Statement of Funeral Goods and Services Selected (Statement) is an itemized list of the goods and services that the consumer has selected during the arrangements conference. The Statement allows consumers to evaluate their selections and to make any desired changes.

Target Market – There are two target markets for this service: older adults and caregivers for older adults (usually their children). A typical older client for ElderCare/PrimePlus Services is someone without an adequate local system of support. This may be because a spouse is deceased or incapacitated, or there are no children living in the area who are capable of, or willing to, assist the parent. Profiling the caregivers, usually adult children, is a more difficult matter. Individually, children may not have sufficient resources, but if they pool their resources, Elder Care Services may be affordable. The markets described above apply to potential clients for the full range of ongoing Elder Care/ Prime Plus Services. The potential market for clients who would benefit from planning for the costs of long-term care and evaluation of care options is much greater. Clients at every income level can benefit from planning for these costs and the earlier a client plans, the greater choices they will have in the future.

Testamentary Trust – A testamentary trust is created by the maker's will, funded by the estate, and administered by a trustee named in the will. Its primary goal is to appoint someone to manage the assets included in the trust. Incidental to this goal is the saving on estate taxes. There are several advantages to using a testamentary trust. One is that the maker can determine how the assets will be paid to the heirs. Sound financial management of the assets may also allow the assets to grow and produce additional income. Also, a by-pass trust may be structured. In this arrangement the spouse can benefit from the trust during their lifetime, in which the principal is held in trust for other beneficiaries. Any remainder, even if it has doubled or tripled in value, produces no new estate taxes because the value of the trust was set for tax purposes at the time of death.

Trusts – Trusts are an important element in the management of a client's estate. Trusts are legal arrangements by which the legal ownership and the beneficial ownership of assets are separated. Trusts can be divided into two major categories, revocable or irrevocable. Irrevocable trusts can not be changed (with very few exceptions) once they are put in place. They can be important in tax planning for larger estates, sometimes taking the form of insurance or a charitable trust. Each can take on many forms or variations. Revocable trusts are one of the most common estate planning tools forindividuals. They can be amended and/or changed at any time before the person making the trust becomes incapacitated or dies. When working with an older client, it is important to continuously review and update any revocable trusts that may exist in order to prevent conflicts and misunderstandings as well as to ensure the client's wishes will be carried out in the event of incapacitation or death.

Viatical Settlements – Viatical settlements refer to situations where an individual sells the benefits of their life insurance policy to a third party at a discount in order to get cash to pay for costly health care services. Viatical settlement companies may pay 60% of the face value of a policy to a person with a life expectancy of two years or less or as much as 80% to an individual with a life expectancy of six months or less. The industry generally uses the term “Viatical Settlement” to refer to a transaction involving a terminally or chronically ill insured and a “Life Settlement” to refer to a transaction involving an insured who is not terminally or chronically ill, generally over the age of sixty-five (65).

Estate, Gift & Trust Planning & Tax Preparation

Federal Estate Tax Update 2002-2010

The Economic Growth and Tax Relief Reconciliation Act of 2001 includes the repeal of federal estate taxes for people dying after December 31, 2009. Between January 1, 2002 and December 31, 2009, the current federal estate tax will gradually decrease as shown in the following table.

![]()

It's very important to be aware that this repeal is temporary; the entire law "sunsets" (expires) after December 31, 2010. This means that the provisions of this 2001 Tax Act will no longer be effective on January 1, 2011 and the tax structure as it existed in 2001 will take effect again (in 2011, Federal estate tax will be assessed on property in excess of $1 million with a maximum tax rate of 55%.)

Gift Tax

Congress did NOT repeal the federal gift tax, although it raised the lifetime gift tax exemption (the amount that may be passed without gift tax) to $1 million, effective in 2002. This means that a person could make a total of $1 million of gifts over his/her lifetime before owing any federal gift tax. Gifts of more than $1 million WILL be taxed, regardless of the exemption for transfers at death. Beginning in 2010, the gift tax rate will equal the highest individual income tax rate (currently scheduled to be 35% in 2010).

Basis of Inherited Property

"Step-up in basis" will continue until December 31, 2009. The "basis" of a piece of property is generally the purchase price of that property and is used to calculate taxable gain when property is sold. The greater the increase in value of property, the greater the taxable gain when sold. A "step-up in basis" means that the basis of inherited property increases to the value of the property on the date of death.

For the year 2010, "step-up" will be replaced by "carry-over basis" rules. Carry-over basis generally means the basis of inherited property remains the same as it was for the deceased owner; which potentially increases the amount of gain (and tax) when the property is sold. When property is inherited, the heir can choose to take a "step-up" in basis for only $1.3 million of the property. For any amount inherited over $1.3 million, the heir's basis will be the smaller of the deceased owner's basis or the date-of-death-market value. The basis of property passing to a surviving spouse can be increased by an additional $3 million.

Basis of property given to the decedent by someone other than his/her spouse within 3 years of death cannot be increased.

Remember, in 2011, step-up in basis generally resumes as it existed prior to this Act, because all provisions of this tax act expire after December 31, 2010.

State Death Tax

Currently, there is a credit against federal estate taxes for death taxes paid to a state. This State death tax credit will be reduced from current levels as follows:

2002 - reduced by 25%

2003 - reduced by 50%

2004 - reduced by 75%

2005 - Completely Repealed

Federal Inheritance Tax is one of those things you really don't feel like dealing with, but in some ways it is part of the cycle of life. Possessions have been passed down from generation to generation throughout history and they provide us with both sentimental and monetary value. Thankfully, we don't have to deal with inheritance issues all the time, but we want to provide that information for those that need it.

Inheritance Tax Law

Depending on where you live the tax code may make reference to inheritance tax, estate tax, and even "death duty." Here in the United States, there is a difference between estate taxes and inheritance taxes. Estate taxes are levied on representatives of the deceased person, while inheritance taxes are levied on the beneficiaries of an estate. Elsewhere in the world, the terms estate tax and inheritance tax are used interchangeably.

Some individuals mistakenly believe that there is a separate inheritance tax rate in the US. IRS tax law, or tax code, does not provide for a special inheritance tax rate, instead there are exemptions and credits that apply to property that is inherited or gifts that are received.

Under the current law, the IRS has a prescribed method for determining if any inheritance tax is due on property or monies received. We are going to briefly describe this method in the section below. Keep in mind that the settling of an estate is a complex matter. An attorney or tax accountant should be consulted in situations where matters of the law are concerned such as the contesting of a Will, known as the probate process.

Inheritance Tax Basis

The first step used to determine any inheritance tax that might be due is to calculate the fair market value of the entire estate. This would include cash, bank accounts, stocks and bonds, real state, insurance, and similar items of value. The total fair market value of all these items is termed the Gross Estate.

Adjustments to Gross Estate

The next step would be to calculate any adjustments to the gross estate. Typical adjustments include paying-off the remaining balance on a mortgage or the fees associated with settling the estate. This last item might include items such as estate administration fees or payments made to an attorney. Finally, there is also a Marital Deduction that can be taken for property that is left to a surviving spouse.

Net Value of Property

Once all the deductions have been taken from the gross estate, the remaining balance is considered the net value of the property - or the inheritance tax basis. To calculate whether nor not any inheritance tax is due; the net value of the property must be subtracted from the inheritance tax credits appearing in the tables below. If the net estate is larger than the tax exclusion, then the federal income taxes due can be found on the standard tax brackets or tax rate tables published by the IRS.

Taxing of Life Insurance Proceeds

Life insurance proceeds paid to you are used in the calculation of the gross estate. The value of any insurance received is subject to the unified credits and inheritance tax exemptions explained later. This last statement is true if you elect to receive the proceeds in the form of a single lump sum.

If you elect to receive life insurance proceeds in installments, then you need to separate the value of the insurance inherited from the total of all payments to determine your federal tax liability. For example, you may be able to elect to receive a lump sum of $100,000 or $10,000 per month for 12 months. The difference between the lump sum payment and the money received is due to interest you are earning on the policy by taking installments.

In this example, you are receiving a total of 12 x $10,000 or $120,000, which is $20,000 higher than the lump sum of $100,000. This means that you would need to pay income tax on the $20,000 received in the form of interest income.

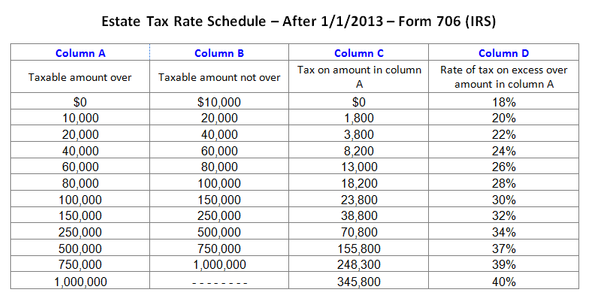

Unified Credits, Gift Tax and Estate Tax

The Unified Credit is used to eliminate or reduce your tax liability. The credit applies to both gifts you may have received and estates that have been inherited. The credit is termed a lifetime credit because as it is consumed by each gift or estate inherited the credit is reduced. The lifetime credit applies to all inheritance or gifts received since 1977.

Under the current law, the gift tax exclusion or credit is separated from the estate tax or credit. For example, the table below indicates the following:

- The lifetime gift tax exclusion you can take in 2009 is $1,000,000. Another way of looking at the same information is to state that you have a $345,800 tax credit that you can apply to any income taxes owed on gifts.

![]()

These inheritance tax tables are used to determine the federally-taxable portion of your inheritance. As previously mentioned, they apply to the net estate you've inherited - not the gross estate or fair market value. Estate taxes are due nine months following the passing of the original property owner. The estate will be settled when a closing letter from the IRS is received confirming the acceptance of the tax forms submitted.

Again, if the estate is large enough to qualify for inheritance tax, the advice of an attorney or accountant specializing in estate taxes should be consulted. Additional information on this topic can be also found on the IRS website.

Estate Planning

ESTATE PLANNING OVERVIEW

If you think estate planning is only for the very rich, you're wrong. Certainly larger estates are subject to large taxes, but taxes are only one reason for estate planning. Here are seven more, some of which may be more important to you:

1. Plan who receives what size share of your assets.

2. Decide how and when your beneficiaries will receive their inheritance or income.

3. Decide who will manage your estate (executor, trustee, etc.) and be responsible for distribution of the assets.

4. Reduce estate administrative expenses and delays.

5. Select a guardian for your children.

6. Provide financial management for funds that may pass to grandchildren.

7. Provide for the orderly continuance or sale of a family business or investment real estate property.

If you don't have a plan, state laws will determine who inherits your assets and when they receive them. The court will appoint a guardian for your children and the administrator for your estate. Your estate could wind up paying a substantial amount of unnecessary taxes and administrative costs,

WHAT ABOUT TAXES?

Settlement expenses and probate costs are an important aspect of estate planning. So are federal and state taxes. While taxes aren't the only estate planning consideration, because they can be so expensive, they are an important one. If your taxable estate exceeds $625,000, your estate is subject to marginal tax federal rates starting at 37% and going as high as 55%. A $2 million taxable estate would be subject to estate taxes of close to $600,000. After 1998, the minimum subject to federal estate taxes is scheduled for small annual adjustments.

The size of your estate is increased by the death benefit of all life insurance you own as well as any court settlements payable as part of a "wrongful death" action.

Planning your estate is about caring for your loved ones, seeing that they are provided for, and making sure your hard earned property is distributed according to your wishes. Your estate consists of all your property including:

- Your business, your home, and other real estate,

- Tangible personal property such as cars and furniture, and

- Intangible property like insurance, bank accounts, stocks, bonds, pension & social security benefits.

An estate plan is your mapping of where you want your property to go after you die.

Not Just For The Older Generation

To many young and middle-aged people die, without warning, often leaving spouse and minor children who need care and direction. Estate planning should be part of your overall financial plan, along with your children's college tuition and your retirement needs. If your circumstances change, it's easy & inexpensive to adjust plans.

What Happens If You Do Not Plan?

If you die without a will or trust, you have in effect left it to your states law to write your will for you. That means the state will make certain assumption about where you would like your money to go to (with which you might not agree). Some of your hard earned money might end up with people who do not need it.

Meanwhile others who might need money more; or who are more deserving, could be shortchanged. Surviving relatives may squabble over who gets particular items of your property, since you did not, make the decisions before death.

Ten Things An Estate Planner Can Do For You

1.Provide for your immediate family

Couples want to provide enough money for their surviving spouse. Couples with children want to assure their education & upbringing. If you have children under 18, both you & your spouse should have a will nominating personal guardians for the children, in case you both should die before, they grow up. Otherwise, a Court will decide without your imput where your kids will live and who will make important decisions about their money, education,& way of life.

2.Get your property to beneficiaries quickly

Options include insurance paid directly to beneficiaries, joint tenancy, personal residence trust, & living trusts, as well as using simplified or expedited probate & taking advantage of laws that provide partial payments to beneficiaries while will is in probate.

3.Plan for incapacity

During estate planning you can also plan for possible mental or physical incapacity. Living wills & durable healthcare powers of attorney enable you to make decisions about life support & pick someone to make your medical treatment choices.

4.Minimize expenses

Good estate planning can keep the cost of transferring property to beneficiaries as low as possible leaving more money for beneficiaries.

5.Choosing executors / trustees for estate

Choosing competent executors/ trustees & giving them the necessary authority will save money, reduce the burden on your survivors, & simplify estate administration. We provide services in this area.

6.Ease the strain on your family

You can take burden from your grieving survivors & plan your funeral arrangement when planning your estate. You may want to simply limit the expense of your burial or designate its place.

7.Help a favorite cause

Your estate plan can help support religious, educational & other charitable causes, either during your lifetime or upon your death, & at the same time take advantage of tax laws designed to encourage private philanthropy.

8.Reduce tax on your estate

Every dollar your estate pays in estate or inheritance taxes is a dollar that your beneficiaries will not receive. A good estate plan can give the maximum allowed by law to your beneficiaries & the minimum to the government.

9.Provide for people who need help & guidance

Do you have an elderly parent or disabled child, or grandchild whose education or health you want to assure. You could establish a special trust fund for family members who need support that you will not be there to provide.

10.Make sure your business goes on smoothly

If you have a small business, you can provide for an orderly succession & continuation of its affairs by spelling out what will happen to business. By using family trusts you can still control your assets & at the same time transfer appreciated property to the next generation.

By our valuing your business you can take advantage of valuation discounts thus reducing your taxable estate by 35 - 45%.

We do all of the Estate Planning and prepare will and all necessary trust documents.

THE ABOVE IMFORMATION FOCUSES ON BROAD LEGAL PRINCIPLES, AND THE INFORMATION PROVIDED SHOULD NOT BE ACTED ON WITHOUT PROFESSIONAL ADVICE. MAKE SURE THE PROFESSIONAL YOU USE IS THROROUGHLY FAMILIAR WITH THE LAW IN YOUR STATE.

Living Wills and health-care Proxies

What is a health-care proxy?

Under New York law, an individual may appoint someone she trusts E.g. a family member or close friend to decide about treatment if she loses ability to decide for herself. She can do this by using a health-care proxy in which she appoint a health care agent to make sure that health-care providers follow her wishes. Her agent can also decide how her wishes apply as her medical condition changes. Hospitals, nursing homes, doctors and other health-care professionals must follow the agent's decisions as if they were the patient's. The individual can give her health-care agent as little or as much authority as she wants. She can allow the agent to decide about all health-care or only certain treatments. To properly protect patient who does not want to be kept alive by machine you must include both a "Do Not Resuscitate" and a "Do Not Intervene" order in all Powers and Living Wills. You must have multiple copies of this document e.g. Patient going to hospital by ambulance. Without DNI, patient could be put on machines and may not be able to be taken off.

What is the difference between a living will and health-care proxy?.

A Living Will is a written statement of an individual's wishes regarding medical treatment. The statement is to be followed if an individual is unable to provide instructions at time medical decisions need to be made. Health-Care proxy is significantly different from Living-Will in that it empowers another person (agent) to make health decisions if patient cannot do so herself/himself. Living-Will on the other hand, has no such provision but enables a person to express his/her own choices regarding medical treatment. It makes sense to utilize both a Living-Will and a Health-Care proxy.

Can the health-care agent be legally or financially liable for health-care decisions made on your behalf?

No. A Health-Care agent will not be liable for treatment decisions made in good faith. The agent cannot be held liable for costs of care just because she/he is an agent.

Do you have to write an advance directive?

No. Signing a Living-Will or Health-Care proxy is voluntary. No one can require an individual to complete documents

Guardianship - A Valuable Legal Tool

In 1993, NYS enacted a new guardianship statute know as Article 81 of the Mental Hygiene Law. The new law set aside the former system of conservatorships and committees. Under Article 81 a court may appoint a guardian for a person whenever it finds by "clear and convincing" evidence that alleged incapacitated person, the "AIP" (1) cannot adequately understand and appreciate nature and consequences of his/her particular limitations and (2) is likely to suffer harm because of these limitations and inability to appreciate consequences. A guardian is a person appointed by Court who receives authority from Court to make certain personal care decisions and/or property and financial mgt. decisions for AIP for a period of time found by Court to be necessary to meet a person's needs. Powers of guardian are specifically limited to those necessary to meet needs of the AIP. A guardian may be an individual of 18 years of age or a parent under 18 years of age and certain public agencies and not-for-profit corporations.

Statute provides that guardian's authority should be tailored to satisfy specific personal and/or property management needs of AIP making available least restrictive form of intervention. In contrast to the old guardianship law under Articles 78 and 81 of the Mental Hygiene Law, the new statute permits AIP as much latitude as possible under circumstances for exercise of independence and self-determination. Guardianship proceeding may be commenced by alleged incapacitated person or a person with whom that person resides, relatives, a trustee of a trust established by and/or for benefit of a person and in fact, any individual who is concerned about welfare of person alleged to be incapacitated.

Eldercare Planning

How and When to Use the Durable Power-of-Attorney

This is one of the most powerful planning tools for estate planning, as well as for Medicaid and other public benefit planning.

When a person (the principal) signs a power-of-attorney, he/she gives another person, (the agent) the power to act in his/her place and on his/her behalf in managing his/her assets and affairs. Agent's powers may be broad and sweeping as to include almost any act, which the principal might have performed. It should be noted however, that in general, acts which are inherently testamentary in nature, such as the authority to make or revoke a will may not be performed by an agent.

A power-of-attorney can be either a "general" power of attorney, where an agent may perform almost any act principal that might have performed himself regarding financial management of his affairs or a "limited" power-of-attorney where the agent has one or more specific powers, such as; power to sell a particular property to particular purchaser at a particular time. Single principal may name one or more agents who can be authorized to act either "jointly" or "severally" (alone without other agent signature).

"Durable power-of-attorney" is unlike normal power-of-attorney which becomes inoperative upon incapacity of principal. Durable power-of-attorney, provides that those powers granted to agent shall not be affected by the subsequent disability or incapacity of principal or by lapse of time.

In most states, in planning for asset management, you should consider granting to agent other important specific powers in addition to those enumerated by statute and found on conventional pre-printed form power-of-attorney. Unless such additional powers are specifically drafted into document, the agent will have no authority to act. Following are a few of many specific powers which a principal should consider including in power-of-attorney: Power to make gifts; change the principal's domicile to a state where Medicaid rules are more favorable; access to safe-deposit boxes; to renounce or disclaim an inheritance and/or insurance proceeds; ability to sign tax returns and IRS powers-of-attorney; to set up and fund trusts and amend existing trusts. In drafting power-of-attorney's, care should be given to confer powers with as much specificity as possible to avoid possibility of a court construing a specific omission as intent to fail to grant that specific power. Such an adverse finding could be a serious detriment to assets.

Advantages for Seriously Ill

Power-of-attorney for asset management in case of a seriously-ill or disabled person is especially useful in situations where a person's assets may be modest and accordingly, do not want warrant expense associated with other planning techniques such as trusts or guardianships.

A great advantage of durable power-of-attorney is that it remains effective after the principal's incapacity. An Agent can act immediately upon principal's incapacity to manage his/her assets or take various measures without initiating costly and time consuming guardianship proceeding to obtain the court's authorization for transactions.

Health - Care Considerations:

In a few states, a principal is allowed to delegate to an agent a durable POA, various health care powers, in addition to control over financial matters. In New York, however, a health-car power-of-attorney, must be a separate document from a power-of-attorney.

Long-term Care

Living Wills and health-care Proxies

What is a health-care proxy?

Under New York law, an individual may appoint someone she trusts E.g. a family member or close friend to decide about treatment if she loses ability to decide for herself. She can do this by using a health-care proxy in which she appoint a health care agent to make sure that health-care providers follow her wishes. Her agent can also decide how her wishes apply as her medical condition changes. Hospitals, nursing homes, doctors and other health-care professionals must follow the agent's decisions as if they were the patient's. The individual can give her health-care agent as little or as much authority as she wants. She can allow the agent to decide about all health-care or only certain treatments. To properly protect patient who does not want to be kept alive by machine you must include both a "Do Not Resuscitate" and a "Do Not Intervene" order in all Powers and Living Wills. You must have multiple copies of this document e.g. Patient going to hospital by ambulance. Without DNI, patient could be put on machines and may not be able to be taken off.

What is the difference between a living will and health-care proxy?.

A Living Will is a written statement of an individual's wishes regarding medical treatment. The statement is to be followed if an individual is unable to provide instructions at time medical decisions need to be made. Health-Care proxy is significantly different from Living-Will in that it empowers another person (agent) to make health decisions if patient cannot do so herself/himself. Living-Will on the other hand, has no such provision but enables a person to express his/her own choices regarding medical treatment. It makes sense to utilize both a Living-Will and a Health-Care proxy.

Can the health-care agent be legally or financially liable for health-care decisions made on your behalf?

No. A Health-Care agent will not be liable for treatment decisions made in good faith. The agent cannot be held liable for costs of care just because she/he is an agent.

Do you have to write an advance directive?

No. Signing a Living-Will or Health-Care proxy is voluntary. No one can require an individual to complete documents

Guardianship - A Valuable Legal Tool

In 1993, NYS enacted a new guardianship statute know as Article 81 of the Mental Hygiene Law. The new law set aside the former system of conservatorships and committees. Under Article 81 a court may appoint a guardian for a person whenever it finds by "clear and convincing" evidence that alleged incapacitated person, the "AIP" (1) cannot adequately understand and appreciate nature and consequences of his/her particular limitations and (2) is likely to suffer harm because of these limitations and inability to appreciate consequences. A guardian is a person appointed by Court who receives authority from Court to make certain personal care decisions and/or property and financial mgt. decisions for AIP for a period of time found by Court to be necessary to meet a person's needs. Powers of guardian are specifically limited to those necessary to meet needs of the AIP. A guardian may be an individual of 18 years of age or a parent under 18 years of age and certain public agencies and not-for-profit corporations.

Statute provides that guardian's authority should be tailored to satisfy specific personal and/or property management needs of AIP making available least restrictive form of intervention. In contrast to the old guardianship law under Articles 78 and 81 of the Mental Hygiene Law, the new statute permits AIP as much latitude as possible under circumstances for exercise of independence and self-determination. Guardianship proceeding may be commenced by alleged incapacitated person or a person with whom that person resides, relatives, a trustee of a trust established by and/or for benefit of a person and in fact, any individual who is concerned about welfare of person alleged to be incapacitated.

$ Monetary Services

We handle complex and sophisticated matters locally, nationally and internationally. We pride ourselves at being accessible, efficient, responsive and technologically sophisticated. In addition, our firms are committed to communities by providing extensive and worthy pro bono and public service. The staffs are by desire actively involved in leadership throughout each firm and with each other. We encourage a commitment to ourselves by sustaining an enriching environment through diversity and teamwork. The firms strive to improve while celebrating their accomplishments, and at the same time providing career opportunities by sustaining growth and financial strength.

Business Succession Planning

Transfers Of Assets To Successor(s)

If you plan to transfer ownership of your business, you will want to ensure the financial security of your retirement. as well as the continued well-being of the business which is the funding vehicle. It is important to have a succession plan for the following reasons:

- you plan to retire but have no immediate successor.

- your designated successor needs more training to operate the business effectively

- your retirement plans have changed

- your designated successor lacks the financial resources required to keep the business running

Proper planning for business succession will ensure the continuation of operations with minimal disruptions because of our tax, business valuation and business expertise. We are capable of creating an all inclusive plan for successfully passing of your business to the next owner, with minimized tax consequences.

The Planning Process

Planning for business succession usually begins with a preliminary evaluation. We gain an understanding of the business and determine whether the succession plan will meet the real objectives of the business & its owner(s). We will research the history & operations of the business. The engagement may consist of client and key personnel interviews, review of financial statements & tax returns. We will also review other relevant documents including trust agreements, wills, shareholder, buy-sell agreements, and partnership agreements.

Developing A Succession Plan

There are four basic stages involved in developing a business succession plan. We possess requisite knowledge and experience to create a plan that is both workable & economically feasible:

1. Fact Finding

We collects information through interviews & the review of Company documents to understand the goals of the owner, the owner's family members, key employees, & the business itself. Specifically the following items need to be examined.

Documents

Interviews of appropriate people and review of important materials.

Financial statements and tax returns

Industry data and trends

Company's business plan

Owner's Information

Specific ideas about succession

Opinions on family members

Strategic plans

Timetable for succession

Family Information

Background and potential successors

Family agreements

Job descriptions and compensation agreements

Key Employee Information

Feedback on current performance and future potential to business

Assessment of capabilities of potential successors

2.Succession

Herein, we considers a number of possibilities with regard to the individuals involved & the advantages & disadvantages of each alternative in terms of business growth.

Some of the most common alternatives:

A Plan For Family Succession

The older generation strongly desires that the younger family members continue to control and operate the business. If training is needed, a CEO can be installed temporarily until the designated family member can properly manage the business.

Sale To Key Employee(s)

The employee(s) need to have the financial resources to acquire the business as well as the management capabilities. Any potential conflict among employees should be resolved.

The Establishment Of An Employee Stock Option Plan(ESOP).

Each year the company contributes a portion of its earnings to the ESOP to enable employees to buy a percentage of the Company's stock.

The Installation Of A New Ceo.

To retain ownership, a board of directors is created to select a CEO to run the business. This can be useful if the owner believes the value of the business will significantly increase.

3.Communicating Findings & Recommendations

Thru fact findings we form the basis of recommendations for action or we may help the you reach a decision.

4.Implementing The Succession Plan

We work with the CEO and/or key personnel to develop a detailed succession plan with milestone dates. We monitor the implementation schedule & act as a liaison between your client and other parties, including bankers, attorneys, investors & family members, in the follow-thru and the training per formulated plan.

Why Choose Our Firm?

We are CPA's, Financial Planners & our owner is a CVA, ( licensed business valuer).

Developing a succession plan requires an analysis of various data on your operations, finances & objectives & the management capabilities of family members. Based on our broad background and expertise in multiple financial and business matters, we are particularly qualified to guide you through each stage of succession planning.

Do to our simultaneous view of your succession needs, by one person, with multiple licenses and business expertise we can help you:

- Gather necessary background information on the company and conduct interviews.

- Clarify your goals and those of key employees.

- Interview and evaluate potential successors.

- Analyze alternative succession plans to determine their advantages and disadvantages.

- Develop a written succession plan and document the necessary skills to operate the business.

- Plan a succession training program in advance of the owner's retirement.

- Create a contingent plan for unexpected situations.

By blending our expertise in business valuation, financial planning, tax & business matters with your company's goals, we can facilitate an orderly transfer of ownership & mgt. of the company, as well as minimize the amount of estate taxes due. Due to our licensed business valuation skills our firm can also help you obtain a reasonable sales price to assist you in maintaining financial independence during your retirement years. Before you make any business decisions contact Sy Schnur CPA's, CVA & Consultants Associated.

Business Restructuring, Mergers, Acquisitions & Business Sale

Restructuring your business — reorganizing your employees, products and financials

- Is in financial or legal distress.

- Wants to re-focus its core business holdings.

- Needs to adapt to rapid growth and organizational change.

Action Steps

- Evaluate your problems - Analyze your situation to determine if your problems have solutions. Are your company's ailments a symptom of its organization, or are they a sign that your business simply isn't viable? Restructuring can save a salvageable business, but it can't help a failed idea succeed.

- Develop a plan - Create a restructuring plan with which to grow your business and consolidate it. Share the plan with your managers, staff and important third parties, including your creditors and vendors.

- Realign your team - Restructuring should include reorganization of your employees. Start at the top with an evaluation of your management team and work your way down the company totem pole. Replace weak members of your team and eliminate extraneous positions.

- Restructure your debts - Use the restructuring process to put your finances in order. Take out new loans, if necessary, to fund restructuring, but work with your accountant to make sure your fiscal plans are sound.

Tips & Tactics

- Lower costs by building intimate relationships with a small number of vendors. Keep them abreast of your company's changes and work with them to maintain affordable service as you move forward with reorganization.

- Restructuring can be as simple as moving things around; be willing to shift financial and personnel resources from less profitable projects to those that make you the most money.

- As you restructure, maintain high customer service standards by answering clients' questions promptly and honestly. Instead of hiding changes from your customers, use restructuring as a means for communicating with them.

- Consider strategic restructuring, whereby you'll partner with another business - via a merger or joint venture, for instance - in order to save yours.

- A restructured company needs entirely new policies and procedures. Wipe your slate clean and meet with remaining employees often to present company goals and get input on company culture.

The economy today is not stabilized. Even big companies have to confront the ups and downs that come their way. But the only thing that keeps them going is survival. They have to survive in the market and progress swiftly or gradually. One strategy to advancement is that of mergers between companies. There are numerous mergers that take place locally but they do not have a great effect on the market especially the consumers. But the mergers that take place at the national or international level have a profound impact on the economies of the concerned countries.

There are different reasons behind a merger of two or more companies. But first of all there exist diverse types of mergers.

a) Horizontal Mergers - two competing companies conjoin to form a single large company. The companies in horizontal mergers are selling the same product in the same market and so are contenders to each other. Such a merger can have a tremendous influence on the market from creating monopoly to escalating prices of the commodity.

b) Commission - the market and the consumers keep a hawks eye on such mergers and at times detains the companies from merging in the interest of the people.

c) The Vertical Mergers - are the mergers between a supplier and the distributor company of the supplies. This is an anti competitive merger but can be highly beneficial to the company. It is because the distributor will no more have to pay for the manufacturing of the supplies, it gets the product at the base price. So there is good cost saving due to this. Vertical merger also rules out lot of competition from the market.

d) Market Extension Merger - between the companies selling same product but in different markets. This merger enhances the market for the two companies since they now act as one sole company.

e) Product Extension Merger is like the one between an eminent company making motor parts and another that makes their own cars. So, the companies involved here sell different but more or less the same product in the same market. This merger promotes the sale of both the companies significantly.

f) Conglomeration is a merger where the concerned companies have nothing in common to sell.

There are various reasons behind merger of companies.

a) Synergy factor prompts the merger of most of the companies. The synergy in business pertains to the cost saving and revenue enhancement. The companies after merger decrease the staff keeping only the skilled labor, work with a single managing director, CEO etc. So there is good outlay saving. Moreover the economy of the sale i.e. the purchasing power of the company booms after merger.

b) To increase the output and rule the market- many mergers are made with the intention to oust the competition and jointly rule the market. This presupposes healthy relations between the competing companies.

c) Mergers also take place when a company is not able to perform well due to some or the other cause like the lack of required investment in the form of capital, tremendous competition etc. In such a situation this company can merge with one its parent company or any other company that has faith in the prior goodwill of the declining company and in its potential to grow and enhance. So companies also merge in order to overcome their internal inconsistencies.

d) Many a mergers besides economically are also politically driven.

e) Acquisitions which imply taking over of one stronger company with the other weaker one are also at times veiled by the name of merger.

However, the directors who plan to merge their companies should actually contemplate over it, keeping in mind all the possible pros and cons. They must seek advice from neutral financial consultants who do are more inclined towards the welfare of the company and not their own. Their own benefit is also hidden in a merger since the wages of the employees increase with the advancement due to merger. So it is recommended to take advice from all those who are the well wishers of the company before taking any concrete step in this direction.

Insurance Monetary Services

For our wealth management client services, including all types of securities products, annuities and insurance investment products, please visit us at www.SyFinance.com

Social Security, Medicare & Medicaid

- If you were married at least 10 years and you are single and age 62 or older, consider claiming Social Security retirement benefits based on your divorced spouse's earnings record. Use this strategy if it would produce a benefit higher than the entitlement based on your own earnings record. If you have been divorced at least two years, you can collect this benefit even though your ex-spouse has not applied.

- If your ex-spouse is deceased and you were married at least ten years, apply for survivor's Social Security benefits at age 60. You must be single to qualify for this benefit or you must have married your present spouse after age 60.

- If you are a divorced parent and you have a child under age 16, apply for Social Security benefits if your divorced wage earner spouse dies, is disabled, or retires and is eligible for Social Security retirement benefits. You will be eligible as long as you were married at least nine months.

- If your ex-spouse is deceased and you were married at least ten years, apply for Medicare at age 65.

Medicaid -Introduction to the Program

Medicaid is a joint federal/ state program providing medical assistance to people meeting certain income and resource limits. It is a health care program covering Prescription drugs, commun-ity based day care, respondent services, in - home care, hospital care & nursing-home care. Medicaid is primary source of funding for long-term custodial care in New York.

Eligibility-Basic Medicaid

Broadly speaking, to be eligible for Medicaid in the community an individual in 2016 may not have more than $ 119,800 in resources and $ 738 in monthly income. If the individual has excess monthly income, he or she is required to contribute that excess to cost of care. Certain burial funds/ prepaid funeral arrangements may be allowed in addition to resource level.

Eligibility for Medicaid in Nursing Home

Same resources limits apply. However, all income for an unmarried individual must be paid onto program to help cover the cost of care, except for the cost of health insurance and a $ 50 monthly needs allowance.

$ From - Well Spouse in a nursing home, law provides resource & income protections for spouse at home ("community spouse") is permitted to retain "spousal share," 1/2 of married couples assets up to maximum of $ 119,800. Not included in calculation of resources is value of home. Additionally, community spouse is allowed a monthly income of $2,019. If community spouse's monthly income is less then $2,019, he / she may draw upon income of nursing- home spouse. In certain circumstances, community spouse's resource & income levels may be increased by a fair- hearing decision or Court order.

In order to be eligible for Medicaid benefits a nursing home resident may have no more than $2,000 in assets (an amount may be somewhat higher in some states). In general, the community spouse may keep one-half of the couple's total "countable" assets up to a maximum of $119,220 (in 2016). Called the "community spouse resource allowance," this is the most that a state may allow a community spouse to retain without a hearing or a court order. The least that a state may allow a community spouse to retain is $23,844 (in 2016).

Example: If a couple has $100,000 in countable assets on the date the applicant enters a nursing home, he or she will be eligible for Medicaid once the couple's assets have been reduced to a combined figure of $52,000 -- $2,000 for the applicant and $50,000 for the community spouse.

Some states, however, are more generous toward the community spouse. In these states, the community spouse may keep up to $119,220 (in 2016), regardless of whether or not this represents half the couple's assets. For example, if the couple had $100,000 in countable assets on the "snapshot" date, the community spouse could keep the entire amount, instead of being limited to half.

The income of the community spouse is not counted in determining the Medicaid applicant’s eligibility. Only income in the applicant’s name is counted. Thus, even if the community spouse is still working and earning, say, $5,000 a month, she will not have to contribute to the cost of caring for her spouse in a nursing home if he is covered by Medicaid. In some states, however, if the community spouse’s income exceeds certain levels, he or she does have to make a monetary contribution towards the cost of the institutionalized spouse’s care. The community spouse’s income is not considered in determining eligibility, but there is a subsequent contribution requirement.

But what if most of the couple's income is in the name of the institutionalized spouse and the community spouse's income is not enough to live on? In such cases, the community spouse is entitled to some or all of the monthly income of the institutionalized spouse. How much the community spouse is entitled to depends on what the Medicaid agency determines to be a minimum income level for the community spouse. This figure, known as the minimum monthly maintenance needs allowance or MMMNA, is calculated for each community spouse according to a complicated formula based on his or her housing costs. The MMMNA may range from a low of $1,991.25 to a high of $2,980.50 a month (in 2016). If the community spouse's own income falls below his or her MMMNA, the shortfall is made up from the nursing home spouse's income.

Example: Joe Smith and his wife Sally Brown have a joint income of $3,000 a month, $1,700 of which is in Mr. Smith's name and $700 is in Ms. Brown's name. Mr. Smith enters a nursing home and applies for Medicaid. The Medicaid agency determines that Ms. Brown's MMMNA is $2,000 (based on her housing costs). Since Ms. Brown's own income is only $700 a month, the Medicaid agency allocates $1,300 of Mr. Smith's income to her support. Since Mr. Smith also may keep a $60-a-month personal needs allowance, his obligation to pay the nursing home is only $340 a month ($1,700 - $1,300 - $60 = $340).

In exceptional circumstances, community spouses may seek an increase in their MMMNAs either by appealing to the state Medicaid agency or by obtaining a court order of spousal support.

Medicaid's Treatment of the Home

Nursing home residents do not automatically have to sell their homes in order to qualify for Medicaid. In some states, the home will not be considered a countable asset for Medicaid eligibility purposes as long as the nursing home resident intends to return home; in other states, the nursing home resident must prove a likelihood of returning home.

But principal residences are not counted as assets by Medicaid only to the extent the applicant's equity interest in the home is less than $552,000, with the states having the option of raising this limit to $828,000 (figures are adjusted annually for inflation; these are for 2016).

The equity value of the home is the fair market value minus any debts secured by the home, such as a mortgage or a home equity loan. For example, if your home has a fair market value of $400,000 and an outstanding mortgage of $100,000, the equity value is $300,000.

But your equity interest depends on whether you own the home by yourself or with someone else. If you own the home by yourself, your equity interest is the entire equity value. If you own your home jointly with your spouse or someone else, your equity interest is only half of the home’s equity value.

The home equity rule does not apply if the Medicaid applicant's spouse or a child who is under 21 or is blind or disabled lives in the home. But the home may be subject to estate recovery<http://www.elderlawanswers.com/medicaids-power-to-recoup-benefits-paid-estate-recovery-and-liens-12018> after the Medicaid recipient’s death, again depending on the state.

$ From - Well Spouse in a nursing home, law provides resource & income protections for spouse at home ("community spouse") is permitted to retain $74,820 or "spousal share," 1/2 of married couples assets up to maximum of $80,760.Not included in calculation of resources is value of home. Additionally, community spouse is allowed a monthly income of $2,019. If community spouse's monthly income is less then $2,019, he / she may draw upon income of nursing- home spouse. In certain circum-stances, community spouse's resource & income levels may be increased by a fair- hearing decision or Court order.

Transfer of Assets

Married individual who require Medicaid may transfer virtually all his or her assets to well spouse, but $ tfr. may be subject to recovery by Medicaid, later. If assets are transferred to persons other than spouse& certain specified individuals, a penalty period is incurred. During that penalty period individual is not eligible for Medicaid nursing home coverage. NOTE: No penalty period for transfer to spouse/ children of assets when applying for Medicaid home care.

Determining Penalty Period

With proper plans maximum period during which an individual may be counted ineligible for Medicaid nursing- home coverage is 36 months for outright transfer & sixty months for transfers to trusts. Penalty periods may be much shorter or, in some cases, avoided entirely!

Record Submission before Acceptance Under Program

When a Medicaid application for nursing-home coverage is made, Medicaid reviews all financial records of applicant & spouse for thirty-six months before month of application to determine whether there were any uncompensated transfers that would incur imposition of penalty period. All uncompensated transfers are added together and total is divided by a number representing the average cost of a nursing home in area where patient is to be institutionalized. Current figure in NYC is $6,521. The result of calculation is the number of months for which the applicant is ineligible for Medicaid coverage in the nursing home. For example, if Mr.Smith. transfers $130,410, to a trust or a nonexempt individual, he will incur a penalty period of 20 months during which time Medicaid will not cover his costs in a nursing home =$130,410/$6,521=20 months.

Transferring a Home

Although individuals home- a house or apartment- is an "exempt" resource for purposes of initial Medicaid eligibility, ultimat-ely it may be subject to a Medicaid demand for reimbursement.

Transfer of home to spouse & certain specified individuals will not trigger a penalty period. However, transfers to any other persons will trigger a penalty period.

Medicaid Trust

Medicaid income only trust is an excellent estate planing tool. This irrevocable trust is funded with assets of a person called a Grantor who retains a life interest funded by invested principal. Grantor has no right to receive any principal distributions. However, trustee whom Grantor appoints is allowed to make gifts of principal to others. In addition to liquid assets such as stocks, bonds & savings accounts, house, cooperative or condominium apartment may also be put into trust with provision that Grantor retain a "life estate," that is, Grantor may continue to live in residence for the remainder of his life.

Medicaid Application for Nursing - Home Coverage