Tax Services ....

- Business Entity Selection, Incorporation & Document Preparation

- Residential & Non-Resident Tax Registration & Tax ID Numbers

- Accounting, Bookkeeping and Write-up Services

- Tax Forms, Organizers & Publications

- Tax Deduction

- Income Taxes and Preparation

- IRS, State and Local Tax Audit and Collection Representation

- Not-for-Profit Formation, Accounting and Income Taxes

- International Taxation

- Estate and Trust Planning and Tax Preparation

- Improving Business Performance

Business Entity Selection, Incorporation & Document Preparation

We prepare the document to form the Sole- Proprietorships, Corporations both C and S, and the LLC entities. Your business entity selection has a large impact on your taxes and other creditor liabilities. From your company's inception through its growth and development, we can advise you on choosing an entity type and later, make changes to another entity time when it is most advantageous. We will incorporate you and prepare all the documents and license forms that you require.

Starting your own business can be a lucrative and rewarding venture. The type of business entity you choose will affect your taxes, personal liability, the size of your company, and how you transfer ownership.

There are five principal business ownership structures for income tax purposes:

- Sole Proprietorship

- Partnership

- C Corporation

- S Corporation

- Limited Liability Company. Publication 583

1. Sole Proprietorship - video

- A sole proprietorship can be appropriate when you, or you and your spouse are the sole owners

- It has the least complicated form of ownership

- It avoids the double taxation of a C corporation

- A sole proprietorship can be appropriate when you are not overly concerned with personal liability

- A proprietorship may be appropriate if your business product or service does not expose you to much risk, and if you have protection provided by malpractice and/or liability insurance.

- Business losses are deductible from your other sources of income.

- Long-term capital gains are subject to a maximum federal tax of 15 %.

- Capital losses are deductible to the extent of capital gains, plus $3,000.

- Expenses of starting up the business are deductible.

- In addition to federal and state income taxes, for 2016 the net income from the business is subject to the Self-Employment Tax at the rate of 15.30% on the first $118,700 and 2.9% on amounts above that.

- See IRS link for futher information

2. Partnership - IRS Publication 541

- A partnership is appropriate when you are in business with an individual other than your spouse.

- It avoids the double taxation of a C Corporation.

- It enables you to divide profits and losses in a ratio that does not correlate with the amounts each partner has invested.

- It provides a business structure that is easy to get started.

- It enables you to split income between family members.

- Business losses are deductible from your personal sources of income depending upon your level of participation in the business.

- Consider a Limited Partnership when:

- The business venture is risky.

- You want to limit your losses to the amount you have invested in the business.

- Your involvement is limited to providing financial backing.

- The organization of the business and the ongoing management is left to others who have the necessary expertise. See Tax Planning: Strategies For Investing In Tax Shelters

- In 2009 a general partner's net earnings from a trade or business are generally is subject to the Self-Employment Tax at the rate of 15.30% on the first $ 106,800 and 2.9% on amounts above that.

3. C Corporation - IRS Publication 542

- The use of a C corporation will provide you with limited personal liability

- It enables you to split income among family members through stock ownership

- Consider a C corporation over a sole proprietorship for maximum tax savings provided that:

- you are in the maximum tax bracket for individuals,

- the corporation plans to save its earnings for future expansion, and

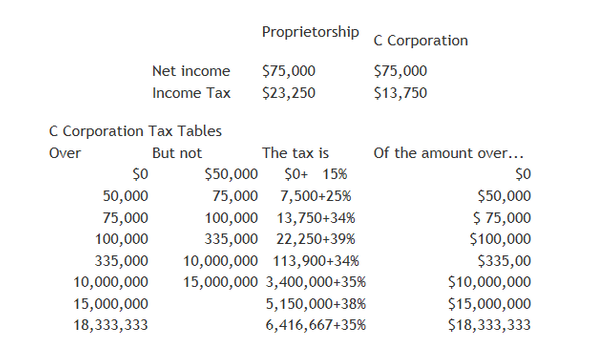

- the taxable income of the business is less than $75,000.

C Corporate Tax Rates

Carl is the sole owner of ABC Company, a sole proprietorship. Carl is personally in the 31% marginal Federal tax bracket. The net income of ABC Company is $75,000. ABC Company plans on using its net income to expand it operations. Carl will save $9,500 in personal income taxes by setting up the business as a C Corporation as opposed to a sole proprietorship.

- If your C Corporation is considered to be a Qualified Personal Service Corporation, all income is taxed at a flat rate of 35 percent. In addition, the tax year-end of the corporation must correspond to the tax year of the owners which is usually December 31. An exception is granted if the corporation can show that there is a valid business purpose for having a different year-end.

A qualified personal service corporation is any corporation: (a) where substantially all of the activities of which involve the performance of services in the fields of health, law, engineering, architecture, accounting, actuarial science, performing arts, or consulting, and (b) at least 95 percent of the stock of which is owned by employees performing the services, retired employees who had performed the services listed above, any estate of an employee or retiree described above, or any person who acquired the stock of the corporation as a result of the death of an employee or retiree described above, if the acquisition occurred within 2 years of death. See Temporary Regulations section 1.448-1T(e) for details.

•You may want to pay the flat 35% tax if you are in the maximum personal tax bracket and if you plan on plowing earnings back into the company.

- Consider a C corporation for the following tax advantages:

- Ability to select a tax year-end other than December 31.

- Tax-free fringe benefits for shareholder-employees, including health care and life insurance.

- Retirement plans that can own the corporation's stock.

- Only 30 percent of dividends received from other corporations are taxable. (Twenty percent if the corporation owns 20 percent or more of the other company.)

- Greater deductibility of losses from tax sheltered investments against the corporations earned income.

- The ability to control when taxable dividends are distributed to shareholders.

- The ability to accumulate at least $250,000 ($150,000 for Personal Service Corporations) without being subject to the unreasonable accumulations tax. Greater amounts can be accumulated if there is a valid business purpose. To the extent income is accumulated within the corporation, double taxation is avoided.

- You can borrow from a C corporation retirement plan. However, if you ever convert to an S corporation be sure the loan is paid off first.

- The major disadvantage of a C corporation from a tax standpoint is the potential for double taxation in the event of a sale of the business. A buyer will likely insist on buying the assets of the business to avoid potential business liabilities and to be able to depreciate or amortize the purchase price. A sale of corporate assets locks the sale proceeds in the C corporation. The proceeds can only be conveyed to the shareholders with a second layer of tax such as in liquidating distribution or a dividend. A sale of C corporation stock will avoid the double taxation problem, but even assuming that the buyer will agree to do this, a knowledgeable buyer will factor in the loss of tax advantages from the asset purchase in setting a lower purchase price for your business. Therefore, when choosing your form of business, you should also consider how you will likely dispose of the business in the future.

Another tax disadvantage is that the tax rate on certain ranges of taxable income is greater than the tax rate for individuals with the same amount of taxable income. Your filing status (married, single, head of household) will have a major impact on what that range of income is. In addition, previously taxed corporate income which is then distributed as a dividend is taxed again. To a certain extent, this problem can be controlled by paying shareholder-employees larger salaries and bonuses. Salaries and bonuses reduce the corporation's taxable income and increase the shareholder-employee taxable income. However, the shareholder-employee's compensation must be reasonable in light of the services rendered.

4. S Corporation IRS Publication 334, IRC 1361

- An S corporation enables you to split income among family members who own stock

- It provides you with limited liability

- It avoids double taxation of income. The net income of the corporation is reportable by the shareholders in the year it is earned.

- Capital gains and losses, and charitable contributions made by the corporation are also passed through to the shareholders.

- Income that is not taken in the form of a salary is not subject to employment taxes. However, the salary must be a reasonable amount in exchange for the services performed. This benefit is particularly valuable in light of the fact that there is no limit on the amount salary that is subject to Medicare taxes.

- Bill earns $400,000 through his S Corporation. By limiting his salary to $100,000, which both Bill and his CPA believe to be reasonable compensation for his services, and reporting $300,000 as a dividend, Bill and the company save $8,700 in Medicare taxes ($300,000 x 2.9%.)

- Losses incurred in non-profitable years are deductible by the shareholders, subject to certain limitations.

- Nontaxable fringe benefits are not available for shareholder-employees owning more than two percent of the stock. Premiums paid for health and accident insurance is taxable income to the owner/employee and also deductible by the corporation. The owner-employee may deduct 60% of the cost in 2001 on page 1 of form 1040. In addition, loans to shareholders from retirement plans are prohibited. Revenue Ruling 91-26, IRC 1372

- Only 75 shareholders are permitted. However, multiple S corporations that operate through a partnership can effectively exceed the 75 shareholder limitation. IRC1361(b)(1)(A), Revenue Ruling 94-43 and Revenue Ruling 77-220

- An unlimited amount of earnings can be accumulated within the S corporation without the imposition of the accumulated earnings tax. The accumulated earnings tax is aimed at C corporations that try to avoid double taxation of earnings (once at the corporate level on net income and again at the shareholder level on the distribution of that income as dividends). You receive an increase in the tax basis of your stock for the amount accumulated which will reduce your taxes should you wish to liquidate the business in the future.

- If you as a shareholder are in the maximum federal tax bracket of 39.6% and your S Corporation is accumulating income for various business needs, you may be better off revoking your S election and paying taxes on the income at the lower C corporation rates. The maximum C corporation rates on taxable income that is less than $15,000,000 is 35%.

- If you plan on selling your business, particularly the assets of the business, an S corporation will only be subject to income tax at the shareholder level. A "C corporation" is subject to income tax at both the corporation level and individual shareholder level.

- S corporations can generate passive income for shareholders that can be used to absorb passive losses from limited partnerships or other passive activities that otherwise would not be deductible due to Section 469 passive activity rules.

- S corporations generally do not pay a corporate level tax on the sale or distribution of appreciated assets. (However, see BIG below.) Sales or distributions do create gains that flow through to the shareholder for taxation. If an S corporation was formerly a C corporation, and the S election was made after 1986, then the S corporation is subject to a corporate level tax on the "build-in gain" (BIG) at the time of the S election. BIG is generally defined as the taxable gain inherent in appreciated property if the asset were sold for its fair market value. BIG also includes certain accrued income items that were not required to be reported as taxable income while a C corporation. Appreciation that occurs after the effective date of the election is not subject to the BIG tax. The S corporation is generally subject to the corporate BIG tax for the 10-year period beginning with the tax year of the S election. The BIG is subject to a flat 35% corporate tax. In addition, the shareholders also pay tax on the BIG. The shareholders are allowed a deduction for the corporation's BIG tax which reduces the impact of the double taxation somewhat.

- An S corporation that has earnings and profits generated when it was formerly a C corporation may also be subject to income tax (flat 35%) on excess net passive income. If excess net passive income occurs for three consecutive years, the S election is terminated. Excess passive income occurs when passive income exceeds 25% of gross receipts. For this purpose, passive income is defined as gross receipts derived from royalties, rents, dividends, interest, , and net capital gain.

- S corporations are not subject to the complex corporate minimum tax rules.

- An S corporation may have an ESOP.

- You can't increase your stock tax basis for commercial loans made to the company. Consequently, losses generated by the corporation in excess of the tax cost of your stock may not be deducted and are suspended until your tax basis is increased. This is generally not the case with a partnership. However, your tax basis will be increased for personal loans you make to your company. IRC 1366 (d)(1)

- Nonresident aliens, corporations, and certain trusts cannot own S corporation stock. S corporations can be held by charitable organizations, retirement plans, and small business trusts.

- Only one class of common stock is allowed. However, common stock can be issued with voting and nonvoting rights.

- Estate planning techniques which employ two classes of stock in an attempt to freeze the value of the company while providing income to the owners is not possible for the S corporation.

- Income and losses must be allocated to shareholders in direct relationship to their stock ownership. Special disproportionate distributions are not permitted.

- For C corporations wishing to elect S corporation status, LIFO inventory reserves must be claimed as income. Any resulting tax is payable by the S corporation over a four-year period. IRC 1363(d)

- The S corporation status can easily be unintentionally revoked which may cause major tax problems. The S status can be revoked for the following reasons: (1) more than 75 shareholders exist, (2) ineligible shareholders, and (3) disproportionate distributions to shareholders (second class of stock). For this reason, it is often advisable to have a stockholders' agreement that restricts transferability to only eligible shareholders and where such additional shareholders will not cause the total to exceed 75. There are also provisions to apply to the IRS for a waiver of inadvertent terminations.

5. Limited Liability Companies

- Limited Liability Companies (LLC) have attributes of both a partnership and a C corporation. All tax consequences pass through to the owners who enjoy the corporate benefit of limited liability. Many states require an LLC to have at least two owners called members. Such an LLC is taxed like a partnership and is not as complex as an S corporation. However, some states will subject an LLC to income tax. Some states permit a single member LLC for which the entity is disregarded for income tax purposes. In this case, the LLC is treated as a sole proprietorship or division of another entity for income tax purposes. Regulation 301.7701-3, Private Letter Ruling 9010027

Residential & Non-Resident Tax Registration & Tax ID Numbers

Any business offering products or services that are taxed in any way must get a federal tax ID number. If your state taxes personal services, or if you are required to collect sales taxes on your sales, you need a federal tax ID number. All the government forms you will be required to file for your business will require either a Social Security number or a tax ID number.

It's safe to say that any business that has employees and/or pays any kind of taxes will need a federal tax ID.

What is an EIN?

An Employer Identification Number (EIN) is a nine-digit number that IRS assigns in the following format: XX-XXXXXXX. It is used to identify the tax accounts of employers and certain others who have no employees. However, for employee plans, an alpha (for example, P) or the plan number (e.g., 003) may follow the EIN. The IRS uses the number to identify taxpayers that are required to file various business tax returns. EINs are used by employers, sole proprietors, corporations, partnerships, non-profit associations, trusts, estates of decedents, government agencies, certain individuals, and other business entities. Use your EIN on all of the items that you send to the IRS and the Social Security Administration (SSA).

Caution: An EIN is for use in connection with your business activities only. Do not use your EIN in place of your social security number (SSN).

You should have only one EIN for the same business entity.

Taxation of Nonresident Aliens

An alien is any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence test.

Who Must File

If you are any of the following, you must file a return:

- A nonresident alien individual engaged or considered to be engaged in a trade or business in the United States during the year. You must file even if:

- Your income did not come from a trade or business conducted in the United States,

- You have no income from U.S. sources, or

- Your income is exempt from income tax.

- However, if your only U.S. source income is wages in an amount less than the personal exemption amount (see Publication 501), you are not required to file.

- A nonresident alien individual not engaged in a trade or business in the United States with U.S. income on which the tax liability was not satisfied by the withholding of tax at the source.

- A representative or agent responsible for filing the return of an individual described in (1) or (2),

- A fiduciary for a nonresident alien estate or trust, or

- A resident or domestic fiduciary, or other person, charged with the care of the person or property of a nonresident individual may be required to file an income tax return for that individual and pay the tax (Refer to Treas. Reg. 1.6012-3(b)).

NOTE: If you were a nonresident alien student, teacher, or trainee who was temporarily present in the United States on an "F,""J,""M," or "Q" visa, you are considered engaged in a trade or business in the United States. You must file Form 1040NR (or Form 1040NR-EZ) only if you have income that is subject to tax, such as wages, tips, scholarship and fellowship grants, dividends, etc. Refer to Foreign Students and Scholars for more information.

Claiming a Refund or Benefit

You must also file an income tax return if you want to:

Claim a refund of overwithheld or overpaid tax, or

Claim the benefit of any deductions or credits. For example, if you have no U.S. business activities but have income from real property that you choose to treat as effectively connected income, you must timely file a true and accurate return to take any allowable deductions against that income.

Which Income to Report

A nonresident alien's income that is subject to U.S. income tax must generally be divided into two categories:

Income that is Effectively Connected with a trade or business in the United States

U.S. source income that is Fixed, Determinable, Annual, or Periodical (FDAP)

Effectively Connected Income, after allowable deductions, is taxed at graduated rates. These are the same rates that apply to U.S. citizens and residents. FDAP income generally consists of passive investment income; however, in theory, it could consist of almost any sort of income. FDAP income is taxed at a flat 30 percent (or lower treaty rate) and no deductions are allowed against such income. Effectively Connected Income should be reported on page one of Form 1040NR. FDAP income should be reported on page four of Form 1040NR.

Which Form to File

Nonresident aliens who are required to file an income tax return must use:

Form 1040NR (PDF) or,

Form 1040NR-EZ (PDF) if qualified. Refer to the Instructions for Form 1040NR-EZ to determine if you qualify.

When and Where To File

If you are an employee or self-employed person and you receive wages or non-employee compensation subject to U.S. income tax withholding, or you have an office or place of business in the United States, you must generally file by the 15th day of the 4th month after your tax year ends. For a person filing using a calendar year this is generally April 15.

If you are not an employee or self-employed person who receives wages or non-employee compensation subject to U.S. income tax withholding, or if you do not have an office or place of business in the United States, you must file by the 15th day of the 6th month after your tax year ends. For a person filing using a calendar year this is generally June 15.

File Form 1040NR-EZ and Form 1040NR at the address shown in the instructions for Form 1040NR-EZ and 1040NR.

Extension of time to file

If you cannot file your return by the due date, you should file Form 4868 (PDF) to request an automatic extension of time to file. You must file Form 4868 by the regular due date of the return.

You Could Lose Your Deductions and Credits

To get the benefit of any allowable deductions or credits, you must timely file a true and accurate income tax return. For this purpose, a return is timely if it is filed within 16 months of the due date just discussed. The Internal Revenue Service has the right to deny deductions and credits on tax returns filed more than 16 months after the due dates of the returns. Refer to When To File in Chapter 7 of Publication 519, U.S. Tax Guide for Aliens (PDF) for additional details.

Departing Alien

Before leaving the United States, all aliens (with certain exceptions) must obtain a certificate of compliance. This document, also popularly known as the sailing permit or departure permit, must be secured from the IRS before leaving the U.S. You will receive a sailing or departure permit after filing a Form 1040-C (PDF) or Form 2063 (PDF).

Even if you have left the United States and filed a Form 1040-C, U.S. Departing Alien Income Tax Return (PDF), on departure, you still must file an annual U.S. income tax return. If you are married and both you and your spouse are required to file, you must each file a separate return, unless one of the spouses is a U.S. citizen or a resident alien, in which case the departing alien could file a joint return with his or her spouse (Refer to Nonresident Spouse Treated as a Resident).

Accounting, Bookkeeping, and write-up services

ACCOUNTING SERVICES

From start-ups to established enterprises, each entity relies on accurate and well setup financial information. This is mandatory in order to see weakness very quickly, maintain profitability and capitalize on new opportunities. Our accounting services steer you closer to these goals with accurate record-keeping and reporting as well as support on financial issues including initial accounting system setup, cost-containment, tax planning, investments, employee benefit and pension planning.

These services include but are not limited to:

- Bookkeeping (Monthly, quarterly, or annually)

- General ledger and financial statement preparation

- Accounting system setup and support

- Payroll and sales tax processing

- Cash flow budgeting and forecasting

- Personal financial statements

- Employee benefit and pension plan planning and implementation

- Investment planning and implementation

- Insurance planning and implementation

- Corporate tax planning and return preparation

- Litigation support

Bookkeeping/Write-up

Accurate record-keeping is essential to a successful business yet can also be complicated and time consuming. Sy Schnur, CPA/PFS can help you with the organization and day-to-day tasks of bookkeeping so that you can focus on your core business.

QuickBooks Accounting Help and Assistance

QuickBooks can provide useful and timely information in the form of financial statements, reports and graphs. However, it can only provide this information if you purchase the right product and then install, setup and use it properly. We don't just help you use software, we help you use it more efficiently and more effectively.

Sy Schnur, CPA/PFS offers the following solutions to help meet your QuickBooks needs:

Personal Training

We train you personally! Either one-on-one or several individuals within your organization at your company's location.

Installation

We install QuickBooks on your stand alone computer or in a network environment, in either single- or multi-user mode.

Setup

We assist new QuickBooks users with initial setup including: Preferences, Lists, Customers, Vendors, Employees, Banking and Reports. We also help experienced users manage their businesses more effectively by improving their current setup. Many users experience problems and lack the ability to generate and track important information as a result of inadequate setup.

Support

Our QuickBooks support service can assist you with any installation, setup or operation assistance you might need. In addition, our support is not limited just to the software part of it, but we can also provide accounting and payroll assistance.

Review

Our QuickBooks review service helps companies that have the human resources to perform daily accounting and payroll tasks, but need an accounting and payroll expert to review your transactions, accounts and reports. This review ensures that you receive timely, relevant and reliable financial information. We also inform you of any corrections, adjustments or reclassifications necessary to ensure that the financial information you receive reflects the correct financial condition of your business. Reviews may be conducted at any time, but monthly reviews provide you with up-to-date information and feedback about your business.

Payroll Services

Sy Schnur, CPA/PFS Income Tax Service's payroll services can help you reduce the time spent on administration through developing and implementing a computerized payroll system that will facilitate processing, timely payment and preparation of tax returns.

Accurate record-keeping is essential to a successful business yet can also be complicated and time consuming. We can help you with the organization and day-to-day tasks of bookkeeping so that you can focus on your core business.

Tax Forms, Organizers and Publications

1. Tax Law Changes Year 2015-2016 - Link

2. How to Prepare Your Tax Record - Link

3. Tax Organizer and Checklist (Click to open)

4. IRS Information Returns , Forms and Instructions - Link

5. International Tax Rates Around the World - Link

INCOME TAX AND PREPARATION

We guide you through full range of tax planning and preparation decisions using planning and strategies that minimize your tax cost. Our expertise, experience, analysis and thorough research allow us to optimize your financial opportunities utilizing existing as well as recently modified and sometimes proposed tax laws.

- WHY HIRE A CPA - Link

- HOW TO PREPARE 1040 - Link

- HOW IRS FINDS UNREPORTED INCOME - Link

- IRS REG. 230 - Link

- CPA ETHICS - Link

State Tax Forms

IRS TAX AUDITS AND TAX BALANCE SETTLEMENTS

We have been doing all types of Federal, State and Local tax audits for the past 50 years. We average only one income tax audit every seven years, while taking very aggressive tax position, within the tax law:

We do a lot of tax audits of all kinds for clients and non-clients and we are extremely successful because of our extensive tax law knowledge and where we can take advantage of loopholes.:

1. Payroll tax audits

2. Sales tax audits

3. Real estate audits and tax certiorari document preparation

4. Income tax audit

5. Income tax appeals

6. Estate and gift tax audits

We work with you on all phases of the audit process making sure we get the best results available under each circumstance.

How an IRS Settlement Works -

Settling Taxes for Less

A partial payment installment agreement allows the taxpayer to enter into an agreement with the IRS to pay back the taxes owed over a specified time and this amount can be less than the total amount initially owed to the IRS. This option is typically available to those individuals that cannot meet the minimum payment amount required with the normal installment agreement.

An installment agreement is the most common method for individuals to pay back IRS taxes owed if they cannot pay in full. Under this form of agreement the taxpayer is allowed to pay back the taxes they owe in monthly payments if they can pay off the entire amount owed in a three year period. This agreement is fairly easy to obtain if an amount of $25,000 or less is owed, if greater, a tax professional will be needed for assistance.

Abate Or Eliminate Penalties

1. Major family problems that you can prove, such as a divorce

2. Theft or destruction of your records

3. A major illness

4. Incarceration or a major disruption to your life

5. Bad advice from a tax expert

6. Disaster that was out of your control (Hurricane, wind storm, flooding, riot, etc.)

7. Lengthy time of unemployment

8. Death of a close family member

9. If for some reason your writing is not practical, you can request an oral interview and you can then state why you qualify for an abatement.

We are heavily experienced with Offer in Compromise or its other name IRS Fresh Start Program.

We work with you on every stage of settlement with the IRS.

1. Working up the Offer, with supporting documentation

2. We you prequalification tools to determine what to Offer so

that it is accepted.

3. If the Offer is rejected and you really do qualify we go to

Appeals on your behalf.

4. We will use bankruptcy laws when necessary to resolve your

situation.

Click here to read about Offer in Compromise with the IRS

Click here to read an article on Refund delays because of Tax Fraud Thieves

Not-for-Profit

Not-for-Profit Formation, Accounting and Income Taxes

We prepare the Form 1023 series of Forms to setup the 501 (c ) Organization. We also file the Form 990, and arrange for the audit process as needed.

Anyone familiar with generally accepted accounting principles and practices will find most accounting for nonprofit activity to be very familiar. There are, however, some significant differences which include:

Accounting for Contributions

Capitalizing and Depreciating Assets

Use of Cash - and Modified Cash-Basis Accounting

Functional Expense Classification

Accounting for Contributions

Nonprofits which qualify for tax exempt status under section 501(c)(3) of the Internal Revenue Code are entitled to receive contributions that are tax deductible to the donor. Since this is unique to the nonprofit sector, there are no equivalent procedures for handling contributions in for-profit accounting. Special procedures have been established for handling the following types of contributions:

Pledges

(Promises to Give) In 1993, the Financial Accounting Standards Board (FASB) issued the Statement of Financial Accounting Standards No. 116, Accounting for Contributions Received and Contributions Made. This Statement sets down firm guidelines for pledge accounting, requiring that legally enforceable, unconditional pledges be recorded in the accounting records. An unconditional pledge is one which is not contingent on some uncertain future event, such as a matching grant from another donor.

Donated Materials and Services

(In-Kind Contributions) FASB Statement No. 116 guidelines also requires that nonprofits account for contributions of most goods (with the exception of works of art and other items held in museum collections). In addition, volunteer time must be included in the financial statements when either:

-The volunteer time results in the creation or enhancement of non-financial assets, such as volunteer labor to renovate a child care center; or

-The services volunteered are specialized skills, such as those provided by accountants, nurses, electricians, teachers, or other professionals and craftsmen.

Special Events and Membership Dues

People who pay to attend fundraisers (such as dinners, auctions, fashion shows, bake sales, etc.) often receive a tangible benefit in return (a meal, a performance, etc.) Similarly, membership dues may entitle individuals to use facilities, receive services, etc. The portion of the special event charge or membership dues which represents the fair market value of the benefit received is not tax deductible to the donor. Some minimal benefits are excluded from this rule.

In addition, the accounting profession has established guidelines for responsibly tracking monies which have been restricted by the donor for a specific use (e.g. buying a new building, starting a new program, adding to the endowment, etc.) How these monies are tracked and reported depends on the nature of the donor''s restriction, what conditions, if any, the donor has imposed on the organization before it can actually receive or use the money, when the restrictions are met, etc.

Capitalizing and Depreciating Assets

As in for-profit accounting, nonprofits are required to record the purchase of long-lasting, substantial property and equipment (such as computers, vans, buildings, etc.) as assets in the financial records, and to charge a portion of the cost of those items in each year in which they have a useful life. This process is called capitalizing and depreciating fixed assets. While all businesses, including nonprofits, are required to record depreciation of assets, some assets in the nonprofit sector receive special treatment. These include museum collections, historical buildings, library books, zoo animals, etc.

Donated items that are added to collections that are held for public exhibition, protected and kept unencumbered, and subject to the policy that, if sold, the proceeds are used to acquire equivalent replacements for the collection, do not have to be recorded as re venue and are not recognized as formal assets in the financial statements.

Use of Cash-and Modified Cash-Basis Accounting

Many small nonprofits use cash-basis rather than accrual-basis accounting to record expenses and revenues. This means that they only record revenue when the cash is received, and only record expenses when they are paid. Some nonprofits use a modified-cash basis of accounting. They will record payroll taxes withheld from employees or large revenue or expense items on an accrual basis. This means recording revenues when they are earned and expenses when obligations are incurred. Most businesses track all expenses and revenue s using accrual accounting.

Functional Expense Allocation

Nonprofits are required to report their expenses by what is known as their functional expense classifications. The two primary functional expense classifications are program services and supporting activities. Supporting activities typically include management and general activities, fundraising, and membership development. Practices vary widely from organization to organization in the nonprofit sector as to how expenses are categorized by functional areas.

Implications of the Differences between Nonprofit and For-Profit Accounting

Because of these few, but significant, differences between nonprofit and for-profit accounting, you will want to select your al personnel, financial advisor, or auditor carefully. The degree to which you receive contributions requiring special handling, or purchase property and equipment covered by special regulations will determine whether you need an accountant who specializes in nonprofit accounting.

In addition, it is important to remember that financial information for nonprofits is interpreted differently from for-profit financial statements. The following is quoted from What a Difference Nonprofits Make: A Guide to Accounting Procedures, 1990, Accountants for the Public Interest.

Meaningful evaluations and comparisons of nonprofit performance almost always prove difficult and complex. While the profitability of two businesses can easily be calculated, it is much harder to compare the effectiveness of two counseling centers to see which is doing a better job of helping the mentally ill. Without the standard of profitability, it is also difficult to compare the job performance of nonprofit staff and managers.

Since the beneficiaries of nonprofits often cannot afford to pay for services, organizations frequently lose money on every sale. As a result, an increase in the number of clients or customers may paradoxically increase the likelihood of a financial crisis. On the other hand, turning a profit may mean that a nonprofit agency has turned away clients, perhaps including the most needy. To determine a nonprofit''s success you must refer to its goals: these are the group''s self-determined replacement for the bottom line of profit-making. The board can measure (a nonprofit''s) success by comparing the results achieved with the results sought.

This points to the importance of a clear mission statement as well as regularly updated short and long-term goals that reflect the purpose of a volunteer agency. It also underscores the need to include service statistics in conjunction with financial statements. In this way, board members can begin to grapple with the complex issues of efficiency and effectiveness as their organization pursues its stated goals.

International Taxation

Whether you're a corporation with overseas operations or a business or individual needing to work out taxation of U.S. residents working abroad. or foreign citizens working in the U.S. or you are going to work abroad, we can help you plot a course through cross-border taxation issues.

International taxation is the study or determination of tax on a person or business subject to the tax laws of different countries or the international aspects of an individual country's tax laws. Governments usually limit the scope of their income taxation in some manner territorially or provide for offsets to taxation relating to extraterritorial income. The manner of limitation generally takes the form of a territorial, residency, or exclusionary system. Some governments have attempted to mitigate the differing limitations of each of these three broad systems by enacting a hybrid system with characteristics of two or more.

Many governments tax individuals and/or enterprises on income. Such systems of taxation vary widely, and there are no broad general rules. These variations create the potential for double taxation (where the same income is taxed by different countries) and no taxation (where income is not taxed by any country). Income tax systems may impose tax on local income only or on worldwide income. Generally, where worldwide income is taxed, reductions of tax or foreign credits are provided for taxes paid to other jurisdictions. Limits are almost universally imposed on such credits. Multinational corporations usually employ international tax specialists, a specialty among both lawyers and accountants, to decrease their worldwide tax liabilities.

With any system of taxation, it is possible to shift or re-characterize income in a manner that reduces taxation. Jurisdictions often impose rules relating to shifting income among commonly controlled parties, often referred to as transfer pricing rules. Residency based systems are subject to taxpayer attempts to defer recognition of income through use of related parties. A few jurisdictions impose rules limiting such deferral (“anti-deferral” regimes). Deferral is also specifically authorized by some governments for particular social purposes or other grounds. Agreements among governments (treaties) often attempt to determine who should be entitled to tax what. Most tax treaties provide for at least a skeleton mechanism for resolution of disputes between the parties.

Contents

1. Introduction

2. Taxation Systems

- 2.1 Territorial

- 2.2 Residency

- 2.3 Exclusion

- 2.4 Hybrid

3. Individuals vs. enterprises

4. Source of income

- 4.1 Definitions of income

- 4.2 Deductions

- 4.3 Thin capitalization

- 4.4 Enterprise restructure

5. Credits for taxes of other jurisdictions

6. Withholding tax

7. Treaties

8. Anti-deferral measures

9. Transfer pricing

10. See also

11. Notes

12. References & Further reading

13. External links

Introduction

Systems of taxation vary among governments, making generalization difficult. Specifics are intended as examples, and relate to particular governments and not broadly recognized multinational rules. Taxes may be levied on varying measures of income, including but not limited to net income under local accounting concepts, gross receipts, gross margins (sales less costs of sale), or specific categories of receipts less specific categories of reductions. Unless otherwise specified, the term “income” should be read broadly.

Jurisdictions often impose different income based levies on enterprises than on individuals. Entities are often taxed in a unified manner on all types of income while individuals are taxed in differing manners depending on the nature or source of the income. Many jurisdictions impose tax at both an entity level and at the owner level on one or more types of enterprises.[1] These jurisdictions often rely on the company law of that jurisdiction or other jurisdictions in determining whether an entity's owners are to be taxed directly on the entity income. However, there are notable exceptions, including U.S. rules characterizing entities independently of legal form.[2]

In order to simplify administration or for other agendas, some governments have imposed “deemed” income regimes. These regimes tax some class of taxpayers according to tax system applicable to other taxpayers but based on a deemed level of income, as if earned by the taxpayer. Disputes can arise regarding what levy is proper. Procedures for dispute resolution vary widely and enforcement issues are far more complicated in the international arena. The ultimate dispute resolution for a taxpayer is to leave the jurisdiction, taking all property that could be seized. For governments, the ultimate resolution may be confiscation of property, dissolution of the entity, or even the death penalty.

Other major conceptual differences can exist between tax systems. These include, but are not limited to, assessment vs. self-assessment means of determining and collecting tax; methods of imposing sanctions for violation; sanctions unique to international aspects of the system; mechanisms for enforcement and collection of tax; and reporting mechanisms.

Taxation Systems

Governments usually limit the scope of their income taxation in some manner territorially or provide for offsets to taxation relating to extraterritorial income. The manner of limitation generally takes one of three forms:

* Territorial: taxation only of in-country income

* Residency: taxation of all income of residents and/or citizens

* Exclusionary: specific inclusion or exclusion of certain amounts, classes, or items of income in/from the base of taxation

Some governments have attempted to mitigate the differing limitations of each of these three broad systems by enacting a hybrid system with characteristics of two or more. For example, they may tax based on residency but provide a specific amount of exclusion for certain foreign income.[3] Alternatively, they may tax income sourced in the country as well as that remitted to the country.[4] Most countries tax gains on dispositions of realty within the country, regardless of residency or their system of taxation.[5]

Territorial

Hong Kong is an example of a territorial tax system.

A few countries tax only income earned within their borders. For example, the Hong Kong Inland Revenue Ordinance imposes income tax only on income earned from a business or source within Hong Kong.[6] Such systems tend to tax residents and nonresidents alike. The key problem argued for this type of territorial system is the ability to avoid taxation on portable income by moving it offshore. This has led governments to enact hybrid systems to recover lost revenue.

Residency

Most income tax systems impose tax on the worldwide income of residents, and impose tax on the income of nonresidents from certain sources within the country. Prime examples of such residency Taxation in the United States and Taxation in the United Kingdom. Residency based systems face the daunting tasks of defining resident and characterizing the income of nonresidents. Such definitions vary by country and type of taxpayer. Examples include:

* The U.S. provides lengthy, detailed rules for individual residency covering:

o Periods establishing residency (including a formulary calculation involving three years)

o Start and end date of residency

o Exceptions for transitory visits, medical conditions, etc.[7]

* UK establishes three categories: non-resident, resident, and resident but not ordinarily resident.[8]

* Switzerland residency may be established by having a permit to be employed in Switzerland for an individual who is so employed.[9]

Exclusion

Many systems provide for specific exclusions from taxable (chargeable) income. For example, several countries, notably Cyprus, Netherlands and Spain, have enacted holding company reigimes that exclude from income dividends from certain foreign subsidiaries of corporations. These systems generally impose tax on other sorts of income, such as interest or royalties, from the same subsidiaries. They also typically have requirements for portion and time of ownership in order to qualify for exclusion. The Netherlands offers a “participation exemption” for dividends from subsidiaries of Netherlands companies. Dividends from all Dutch subsidiaries automatically qualify. For other dividends to qualify, the Dutch shareholder or affiliates must own at least 5% and the subsidiary must be subject to a certain level of income tax locally.[10]

Hybrid

Some governments have chosen, for all or only certain classes of taxpayers, to adopt systems that are a combination of territorial, residency, or exclusionary. There is no pattern to these hybrids. Following are examples:

* The U.S. allows individuals earning income from their personal services outside the U.S. — an exclusion of up to US$80,000 (indexed for inflation from a key date) from compensation for such services. Compensation income in excess of this amount is fully taxable to citizens and residents.[11]

* The UK imposes a charge to tax on individuals “resident but not ordinarily resident” in the UK based on income earned in or remitted to the UK.[12]

* Singapore imposes income tax on resident individuals and companies on all income earned in or remitted to Singapore.[13]

Individuals vs. enterprises

Many tax systems tax individuals in one manner and entities that are not considered fiscally transparent in another. The differences may be as simple as differences in tax rates,[14] and are often motivated by concerns unique to either individuals or corporations. For example, many systems allow taxable income of an individual to be reduced by a fixed amount allowance for other persons supported by the individual (dependents). Such a concept is not relevant for enterprises.

Many systems allow for fiscal transparency of certain forms of enterprise. For example, most countries tax partners of a partnership, rather than the partnership itself, on income of the partnership.[15] A common feature of income taxation is imposition of a levy on certain enterprises in certain forms followed by an additional levy on owners of the enterprise upon distribution of such income. Thus, many countries tax corporations under company tax rules and tax individual shareholders upon corporate distributions. Various countries have tried (and some still maintain) attempts at partial or full “integration” of the enterprise and owner taxation. Where a two level system is present but allows for fiscal transparency of some entities, definitional issues become very important.

Source of income

Determining the source of income is of critical importance in a territorial system, as source often determines whether or not the income is taxed. For example, Hong Kong does not tax residents on dividend income received from a non-Hong Kong corporation.[16] Source of income is also important in residency systems that grant credits for taxes of other jurisdictions. Such credit is often limited either by jurisdiction or to the local tax on overall income from other jurisdictions.

Source of income is where the income is considered to arise under the relevant tax system. The manner of determining the source of income is generally dependent on the nature of income. Income from the performance of services (e.g., wages) is generally treated as arising where the services are performed.[17] Financing income (e.g., interest, dividends) is generally treated as arising where the user of the financing resides.[18] Income related to use of tangible property (e.g., rents) is generally treated as arising where the property is situated.[19] Income related to use of intangible property (e.g., royalties) is generally treated as arising where the property is used. Gains on sale of realty are generally treated as arising where the property is situated.

Gains from sale of tangible personal property are sourced differently in different jurisdictions. The U.S. treats such gains in three distinct manners: a) gain from sale of purchased inventory is sourced based on where title to the goods passes;[20] b) gain from sale of inventory produced by the person (or certain related persons) is sourced 50% based on title passage and 50% based on location of production and certain assets;[21] c) other gains are sourced based on the residence of the seller.[22]

Where differing characterizations of an item of income can result in differing tax results, it is necessary to determine the characterization. Some systems have rules for resolving characterization issues, but in many cases resolution requires judicial intervention.[23] Note that some systems which allow a credit for foreign taxes source income by reference to foreign law.[24]

Definitions of income

Some jurisdictions tax net income as determined under financial accounting concepts of that jurisdiction, with few, if any, modifications.[25] Other jurisdictions determine taxable income without regard to income reported in financial statements.[26] Some jurisdictions compute taxable income by reference to financial statement income with specific categories of adjustments, which can be significant.[27]

A jurisdiction relying on financial statement income tends to place reliance on the judgment of local accountants for determinations of income under locally accepted accounting principles. Often such jurisdictions have a requirement that financial statements be audited by registered accountants who must opine thereon.[28] Some jurisdictions extend the audit requirements to include opining on such tax issues as transfer pricing.[29] Jurisdictions not relying on financial statement income must attempt to define principles of income and expense recognition, asset cost recovery, matching, and other concepts within the tax law. These definitional issues can become very complex. Some jurisdictions following this approach also require business taxpayers to provide a reconciliation of financial statement and taxable incomes.[30]

Deductions

For more details on this topic, see Tax deduction.

Systems that allow a tax deduction of expenses in computing taxable income must provide for rules for allocating such expenses between classes of income. Such classes may be taxable versus non-taxable, or may relate to computations of credits for taxes of other systems (foreign taxes). A system which does not provide such rules is subject to manipulation by potential taxpayers. The manner of allocation of expenses varies. U.S. rules provide for allocation of an expense to a class of income if the expense directly relates to such class, and apportionment of an expense related to multiple classes. Specific rules are provided for certain categories of more fungible expenses, such as interest.[31] By their nature, rules for allocation and apportionment of expenses may become complex. They may incorporate cost accounting or branch accounting principles,[31] or may define new principles.

Thin capitalization

Main article: Thin capitalization

Most jurisdictions provide that taxable income may be reduced by amounts expended as interest on loans. By contrast, most do not provide tax relief for distributions to owners.[32] Thus, an enterprise is motivated to finance its subsidiary enterprises through loans rather than capital. Many jurisdictions have adopted "thin capitalization" rules to limit such charges. Various approaches include limiting deductibility of interest expense to a portion of cash flow,[33] disallowing interest expense on debt in excess of a certain ratio,[34] and other mechanisms.

Enterprise restructure

The organization or reorganization of portions of a multinational enterprise often gives rise to events that, absent rules to the contrary, may be taxable in a particular system. Most systems contain rules preventing recognition of income or loss from certain types of such events. In the simplest form, contribution of business assets to a subsidiary enterprise may, in certain circumstances, be treated as a nontaxable event.[35] Rules on structuring and restructuring tend to be highly complex.

Credits for taxes of other jurisdictions

Further information: Tax credit and Foreign tax credit

Systems that tax income earned outside the system's jurisdiction tend to provide for a unilateral credit or offset for taxes paid to other jurisdictions. Such other jurisdiction taxes are generally referred to within the system as “foreign” taxes. Tax treaties often require this credit. A credit for foreign taxes is subject to manipulation by planners if there are no limits, or weak limits, on such credit. Generally, the credit is at least limited to the tax within the system that the taxpayer would pay on income earned outside the jurisdiction.[36] The credit may be limited by category of income,[37] by other jurisdiction or country, based on an effective tax rate, or otherwise. Where the foreign tax credit is limited, such limitation may involve computation of taxable income from other jurisdictions. Such computations tend to rely heavily on the source of income and allocation of expense rules of the system.[38]

Withholding tax

For more details on this topic, see Withholding.

Many jurisdictions require persons paying amounts to nonresidents to collect tax due from a nonresident with respect to certain income by withholding such tax from such payments and remitting the tax to the government.[39] Such levies are generally referred to as withholding taxes. These requirements are induced because of potential difficulties in collection of the tax from nonresidents. Withholding taxes are often imposed at rates differing from the prevailing income tax rates.[40] Further, the rate of withholding may vary by type of income or type of recipient.[41][42] Generally, withholding taxes are reduced or eliminated under income tax treaties (see below). Generally, withholding taxes are imposed on the gross amount of income, unreduced by expenses.[43] Such taxation provides for great simplicity of administration but can also reduced the taxpayer's awareness of the amount of tax being collected.[44]

Treaties

Main article: Tax treaty

OECD members Accession candidate countries Enhanced engagement countries

Tax treaties exist between many countries on a bilateral basis to prevent double taxation (taxes levied twice on the same income, profit, capital gain, inheritance or other item). In some countries they are also known as double taxation agreements, double tax treaties, or tax information exchange agreements (TIEA).

Most developed countries have a large number of tax treaties, while developing countries are less well represented in the worldwide tax treaty network.[45] The United Kingdom has treaties with more than 110 countries and territories. The United States has treaties with 56 countries (as of February 2007). Tax treaties tend not to exist, or to be of limited application, when either party regards the other as a tax haven. There are a number of model tax treaties published by various national and international bodies, such as the United Nations and the OECD.[46]

Treaties tend to provide reduced rates of taxation on dividends, interest, and royalties. They tend to impose limits on each treaty country in taxing business profits, permitting taxation only in the presence of a permanent establishment in the country.[47] Treaties tend to impose limits on taxation of salaries and other income for performance of services. They also tend to have “tie breaker” clauses for resolving conflicts between residency rules. Nearly all treaties have at least skeletal mechanisms for resolving disputes, generally negotiated between the “competent authority” section of each country's taxing authority.

Anti-deferral measures

Residency systems may provide that residents are not subject to tax on income outside the jurisdiction until that income is remitted to the jurisdiction.[48] Taxpayers in such systems have significant incentives to shift income offshore. Depending on the rules of the system, the shifting may occur by changing the location of activities generating income or by shifting income to separate enterprises owned by the taxpayer. Most residency systems have avoided rules which permit deferring offshore income without shifting it to a subsidiary enterprise due to the potential for manipulation of such rules. Where owners of an enterprise are taxed separately from the enterprise, portable income may be shifted from a taxpayer to a subsidiary enterprise to accomplish deferral or elimination of tax. Such systems tend to have rules to limit such deferral through controlled foreign corporations. Several different approaches have been used by countries for their anti-deferral rules.[49]

In the United States, rules provides that U.S. shareholders of a Controlled Foreign Corporation (CFC) must include their shares of income or investment of E&P by the CFC in U.S. property.[50] U.S. shareholders are U.S. persons owning 10% or more (after the application of complex attribution of ownership rules) of a foreign corporation. Such persons may include individuals, corporations, partnerships, trusts, estates, and other juridical persons. A CFC is a foreign corporation more than 50% owned by U.S. shareholders. This income includes several categories of portable income, including most investment income, certain resale income, and certain services income. Certain exceptions apply, including the exclusion from Subpart F income of CFC income subject to an effective foreign tax rate of 90% or more of the top U.S. tax rate.[50]

The United Kingdom provides that a UK company is taxed currently on the income of its controlled subsidiary companies managed and controlled outside the UK which are subject to “low” foreign taxes.[51] Low tax is determined as actual tax of less than three-fourths of the corresponding UK tax that would be due on the income determined under UK principles. Complexities arise in computing the corresponding UK tax. Further, there are certain exceptions which may permit deferral, including a “white list” of permitted countries and a 90% earnings distribution policy of the controlled company. Further, anti-deferral does not apply where there is no tax avoidance motive.[52]

Rules in Germany provide that a German individual or company shareholder of a foreign corporation may be subject to current German tax on certain passive income earned by the foreign corporation. This provision applies if the foreign corporation is taxed at less than 25% of the passive income, as defined.[citation needed] Japan and some other countries have followed a “black list” approach, where income of subsidiaries in countries identified as tax havens is subject to current tax to the shareholder. Sweden has adopted a “white list” of countries in which subsidiaries may be organized so that the shareholder is not subject to current tax.

Transfer pricing

Main article: Transfer pricing

The setting of the amount of related party charges is commonly referred to as transfer pricing. Many jurisdictions have become sensitive to the potential for shifting profits with transfer pricing, and have adopted rules regulating setting or testing of prices or allowance of deductions or inclusion of income for related party transactions. Many jurisdictions have adopted broadly similar transfer pricing rules. The OECD has adopted (subject to specific country reservations) fairly comprehensive guidelines.[53] These guidelines have been adopted with little modification by many countries.[54] Notably, the U.S. and Canada have adopted rules which depart in some material respects from OECD guidelines, generally by providing more detailed rules.

Arm's length principle: a key concept of most transfer pricing rules is that prices charged between related enterprises should be those which would be charged between unrelated parties dealing at arm's length. Most sets of rules prescribe methods for testing whether prices charged should be considered to meet this standard. Such rules generally involve comparison of related party transactions to similar transactions of unrelated parties (comparable prices or transactions). Various surrogates for such transactions may be allowed. Most guidelines allow the following methods for testing prices: Comparable uncontrolled transaction prices, resale prices based on comparable markups, cost plus a markup, and an enterprise profitability method.

Reporting Requirements for Foreign Assets

What you should know about the new Code Section 6038D. The 2009 Internal Revenue Service (IRS) amnesty program for failure to file Form TD F 90-22.1, “Report of Foreign Bank and Financial Accounts,” (the FBAR), heightened our awareness of the importance of filing information returns disclosing foreign bank accounts. We all reviewed the various IRS pronouncements and notices on FBAR filing requirements. Now we have to learn a whole new filing regime the purpose of which is similar to the purpose of the FBAR.

Section 6038D

The new section, Section 6038D, was added to the Code by the Hiring Incentives to Restore Employment (HIRE) Act (P.L. 111-147), effective for tax years beginning after March 18, 2010. Under new Code Section 6038D, an individual must attach to his or her tax return certain information about “foreign financial assets” if the aggregate value of all the assets exceeds $50,000 (or such higher dollar amount as the Secretary may prescribe). “Foreign financial assets” include any depository, custodial or other financial account maintained by a foreign financial institution and to the extent not held in an account maintained by a financial institution:

I.Any stock or security issued by a person other than a U.S. person,

II.Any financial instrument or contract held for investment that has an issuer or counterparty other than a U.S. person and

III.Any interest in a foreign entity. It is clear that there is overlap between the filing requirements for the FBAR and the information requirements under new Code Section 6038D. The Joint Committee on Taxation in its report (Report No. JCX-4-10) recognized the overlap; however, it also pointed out one example in which an FBAR would not be required, but reporting under Code Section 6038D may be required. That example was the beneficiary of a foreign trust, who is not within the scope of FBAR reporting because their interest in the trust is less than 50 percent, but may be within the scope of Section 6038D if the value of their interest in the trust together with the value of other specified foreign financial assets exceeds the aggregate value threshold. There was much discussion last year regarding whether a foreign hedge fund was a foreign financial account under the FBAR regulations. In Proposed Regulations on FBAR, reporting promulgated in February 2010 that issue was reserved because of pending legislative proposals. Surely new Code Section 6038D was the reason for the reservation.

The consequences of not filing the required information with the tax return are onerous:

1.There is a $10,000 penalty set forth in Code Section 6038D(d)(1). This penalty may be increased if the taxpayer is notified about the failure and does not respond within 90 days after the day the notice is mailed. The increase is $10,000 for each 30-day period (or fraction thereof) during which the failure continues after the expiration of the 90-day period. The penalty cannot exceed $50,000. I.R.C. 6038D(d)(2). The penalty is subject to abatement provided the failure is due to reasonable cause and not willful neglect. I.R.C. 6038D(g).

2.Code Sections 6662(b)(7) and (j) were added under HIRE, which provisions impose a 40-percent accuracy-related penalty for underpayment of tax that is attributable to an “undisclosed foreign financial asset understatement.” A “foreign financial asset understatement” for any tax year is the portion of the understatement for the year that is attributable to any transaction involving an undisclosed foreign financial asset that should have been disclosed under information reporting sections listed in Section 6662(j)(2), on which list Section 6038D is included.

3.Section 6501(c)(8), a provision suspending the Statute of Limitations from running, was amended under HIRE to include Section 6038D and to add “ tax return.” As originally enacted in March 2010, this change prevented the general three-year period for assessment from beginning to run for any item on a tax return until the IRS is provided information required under listed information reporting provisions, including new Section 6038D, even though the item is unrelated to income adjustments associated with missing information requirements. In other words, the Statute of Limitations was kept open for all issues on a taxpayer's return if it fails to report under the listed information reporting Code sections. Fortunately, Section 6501(c)(8) was amended in legislation signed by the President on August 10, 2010 by adding a new provision, Section 6501(c)(8)(B), which provision provides that the failure to attach an information return will only keep the statute open for items on the return relating to the failure provided the taxpayer acted with reasonable cause and not with willful neglect.

4.The substantial omission provision extending the Statute of Limitations from three years to six years, Section 6501(e), was amended to provide that the six-year period applies if there is an omission of gross income in excess of $5,000 and the omitted gross income is attributable to a foreign financial asset with respect to which:

I.InformInformation reporting is required under Code Section 6038D or ation reporting is required under Code Section 6038D or

II.Would be required if Code Section 6038D were applied without regard to the $50,000 aggregate asset value threshold amount and any other exceptions provided by regulations permitted under Section 6038D(h)(1) involving duplicative disclosure of assets.

Code Section 6038D Accomplishments

What has been accomplished by the enactment of Code Section 6038D when compared to the FBAR reporting provisions?

When reading the Joint Committee on Taxation Report (JCX-4-10), it is clear that Congress was frustrated by the fact that the FBAR reporting requirements originate in the Bank Secrecy Act, which is part of Title 31 of the United States Code, versus Title 26, which is the Internal Revenue Code. Although the FBAR is received and processed by the IRS, it is neither part of the income tax return filed with the IRS nor filed in the same office as the return. Accordingly, under Title 26, the FBAR is not considered “return information,” and its distribution to other law enforcement agencies is not limited by the nondisclosure rules of Title 26. Also, the collection and enforcement powers available to enforce the Internal Revenue Code under Title 26 are not available to the IRS in the enforcement of the FBAR civil penalties, which remain collectible only in accord with the procedures for non-tax collections. The only connection between the FBAR and Form 1040 is the question on Schedule B asking the taxpayer about interests in foreign financial accounts and reference to page B-2 for exceptions and filing requirements for Form TD F 90-22.1. Information reported on Schedule B is not readily available to those within the IRS, who are administering FBAR compliance, despite the fact that the Federal return may be the best source of information for this purpose. Furthermore, the FBAR civil penalties are limited to willful failure to comply with FBAR reporting requirements and a reduced penalty for a non-willful, but negligent, failure to file. In contrast, there are various sanctions allowed by the Code for failure to file required information, including suspension of the applicable statute of limitations and penalties based upon underpayment of tax resulting from failure to disclose. The Code penalties impose a lesser burden of proof and threshold for imposition of the penalty than the willful FBAR penalty.

Estate and Trust Planning and Tax Preparation

Large estates are subject to high estate taxes and normally have in depth estate planning. However, planning also determines who receives what share of the estate, how and when the beneficiaries will receive their inheritance and income share, who will be the guardian for your children, who will manage your estate (executor, trustee, etc.) and be responsible for distribution of the assets, who will manage the funds that may pass to grandchildren, who will provide orderly continuance of sale of the family business and who will plan for plan how administrative expenses will be paid without delays.

Improving Business Performance

Restructuring Your Organization for Results!

Benefits Must Outweigh Costs, Including Time to Be Offline!

Warning Signs That Indicate You May Need To Improve The Performance Of Your Business

Telltale Signs -- Where You Might Be In Need Of A Restructuring

Designing a New Structure

Summary Of Where We Can Help You Run You Business More Effectively

Warning Signs That Indicate You May Need To Improve The Performance Of Your Business

A business' success is determined by many items, among which is Company structure including its policies and procedures , personel, systems, & the relationships of the business and all of its ingredients to one another. Building a strong business organization for your Company can result in:

- More Efficiently Planned Operations

- Improved Communications.

- Enhanced Profitability.

- Better Utilization Of Employees' And There Talents.

As companies compete in a tough global marketplace, the CPA's ,the business valuer & the financial planner play important roles as business advisors. In response to our clients' diverse needs, we have developed expertise in such specialized areas as information technology, time management, human resources, operational and production efficiency. Though you know your business better than anyone else, it may be difficult for you to see the weaknesses that could cause its downfall. Our firm brings along the combined expertise, by our being CPA's, computer system technicians, financial planners and certified business valuers. As such we can assist you in identifying problems caused by your organizational structure long before the problems become unresolvable.

Because of our broad experience with financial and business matters, we can help you implement those practical solutions to improve the inefficiency of your business. We are able to provide you with the objective insight you need to create a solid foundation for your company, or in certain cases direct you to other specialized professionals, where there specific abilities are more efficient for the specific problem.

Telltale Signs --Where You Might Be In Need Of A Restructuring. The changing business environment may call for changes in your organizational structure. E.g., if your company has merged with or acquired another company introduced new product line, acquired new technology, or downsized, you will probably need to consider restructuring.

Your organization must have the right people employed in the right places for it to function effectively and profitably. In particular, the following symptoms signal a need for changes within an organization:

•Low Employee Morale

Esprit de corps is missing. Your staff's fears and anxieties about losing their jobs may be reflected in anger toward the total Company, resulting in lower degree of productivity.

•High People Turnover

Continuous personnel changes resulting in increased training costs and low productivity. Management cannot understand the cause.

•High Labor Costs

Labor costs creeping up faster than increase in productivity or sales.

•Inefficient Operations

The Company is unable to handle sudden growth resulting from increased demand for product / service.

•Poor Internal Communications

The owners/managers do not have timely access to data needed to manage the business. One department or person may not know the effect of operations on another department or person within the organization, or what financial commitments are made on its behalf.

•Decreased Profitability

Downward trends in profitability & key financial ratios require a review of the operations for cause.

•Present Performance

A review of your current business performance can provide you with insight on what changes need to be made. Through interviews, questionnaires and observation, we can gather the data needed to evaluate your present organizational structure objectively.

Small Business Stimulus Passes Congress

The House on Thursday passed the Small Business Jobs Act of 2010 (HR 5297) by a vote of 237–187, and sent it to the President, who is expected to sign the bill into law.

The bill, which passed the Senate last week, expands loan programs through the Small Business Administration (SBA), strengthens small business preference programs for federal government projects, provides incentives for exporters, offers a variety of small business tax breaks and includes some revenue raisers.

Small Business Loans

The bill creates a Small Business Lending Fund to address ongoing effects of the financial crisis on small businesses by allowing the Treasury Department to make capital investments in eligible financial institutions to increase credit available for small businesses. Independent community banks may participate in a new $30 billion lending fund on the condition they make loans to small businesses and meet other requirements. Financial institutions (bank and savings and loan holding companies, depository institutions, and community development loan funds) with $10 billion or less in total assets may apply for capital investments of up to 3% of risk-weighted assets.

Other small business lending provisions in the act include:

Online information center. The bill directs the SBA to create an online lending platform that lists all lenders that make SBA-guaranteed loans and provides interest rates for each lender.

Nonprofit lenders pilot. The bill also creates an intermediary lending pilot program to allow certain private, nonprofit entities that seek or have been awarded SBA loans to make loans to small businesses. The pilot will allow $20 million in loans each year from 2011 to 2013 to not more than 20 eligible entities. Eligible nonprofit organizations may apply for up to $1 million for the purpose of lending up to $200,000 to eligible small businesses.

Increased maximums for Microloan Program. The bill increases the Microloan Program maximum loan amount to $50,000 from $35,000. The bill raises total outstanding loan commitment limits to $4.5 million from $1.5 million and the total gross loan amount to $5 million from $2 million. Increased government guarantees and outstanding loan commitments are effective until Jan. 1, 2011, when the percentage guarantees will revert to the original percentages and the total outstanding loan commitment will reduce to $3.75 million.

Increased participation limit for Section 7(a) business loans. It also increases the limit on the government's participation in so-called Section 7(a) small business loans to 90% from 75% or 85% for all Section 7(a) loans regardless of loan amount.